Bayesian Machine Learning

Philosophical Foundations and Bayes’ Theorem¶

Interpretations of probability¶

Frequentist definition: Probability of event is the long-run relative frequency of in infinitely many repetitions of the same experiment. Statements are about data, not parameters ( is defined via an idealized limit of repetitions).

Bayesian definition: Probability is a subjective degree of belief about events or parameters, given current knowledge ( quantifies how plausible you think is).

Key philosophical contrast¶

Frequentist: uncertainty is in the world (randomness of experiments).

Bayesian: uncertainty is in the head of the observer (state of information; different observers with different prior knowledge can have different probabilities).

Sampling vs. inference¶

Sampling (forward problem): Assume parameter is known, ask: “If is the probability of success, what is ?”. For example: Number of heads in 10 tosses with known ~ Binomial().

Inference (inverse problem): Assume data is observed, but the parameters are unknown, ask: “Given I observed heads in 10 tosses, what do I believe about ?”

Frequentist: Estimate single “best” value (e.g. MLE )

Bayesian: derive a posterior distribution over :

Bayes’ theorem and roles of likelihood¶

Bayes’ theorem (discrete):

Belief-updater view:

Prior: beliefs before data.

Likelihood: how plausible data are under different parameter values.

Posterior: updated beliefs after data.

Likelihood in both schools:

In frequentist statistics, the likelihood function is used to perform Maximum Likelihood Estimation (MLE). This identifies the single parameter value that maximizes the probability of having produced the observed data.

In Bayesian statistics, the likelihood function serves as a belief updater. It is multiplied by the prior distribution to calculate the posterior, allowing you to estimate a full distribution of all plausible values rather than just one “best” number.

When Bayesian methods are preferable¶

Small sample sizes / rare events: frequentist asymptotics unreliable.

Strong prior information available (expert opinion, previous studies) and should be integrated.

Need full uncertainty quantification (posterior distributions, credible intervals) rather than point estimates or p-values.

Complex hierarchical or graphical models, where likelihood-based methods get complicated but Bayesian methods remain conceptually coherent.

The computational curse of Bayesian statistics¶

Core difficulty: the evidence (marginal likelihood) is an often intractable integral:

In simple conjugate families this integral is analytic.

In realistic models (many parameters, non-Gaussian likelihoods), high‑dimensional integrals are impossible to compute in closed form.

This computational curse motivates Markov Chain Monte Carlo (MCMC) and Variational Inference.

Conjugate Families and Continuous Inference¶

Conjugate families are pedagogically useful to understand how priors and data trade off.

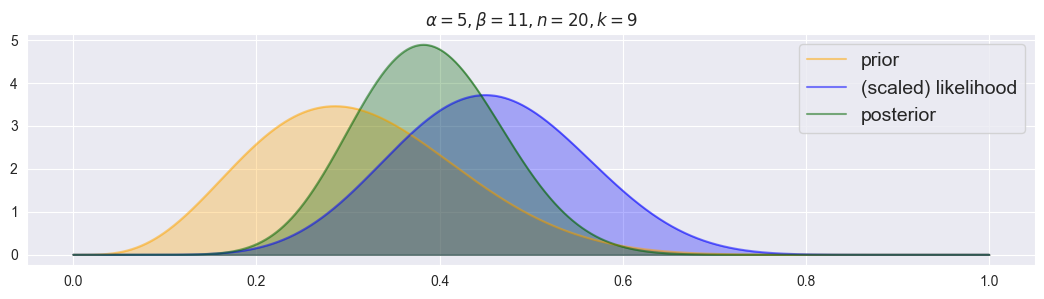

Beta-Binomial¶

Likelihood:

is the binomial coefficient, representing the number of ways to choose successes from trials:

is the probability of getting exactly successes

is the probability of getting exactly failures

Prior:

with:

Posterior:

Key properties: Prior “pseudo-counts”: successes, failures

With more data, likelihood dominates; with little data, prior dominates

Order of data does not matter; only sufficient statistics

Notebook Cell

import numpy as np

import matplotlib.pyplot as plt

from scipy import stats

def plot_beta_binomial( alpha, beta, n, k, figsize=(13,3) ):

# create figure

plt.figure( figsize=figsize )

# numeric evaluation range for pi

pi_range = np.linspace(0, 1, 1000)

# prior

prior = [stats.beta.pdf(pi, a=alpha, b=beta) for pi in pi_range]

plt.plot( pi_range, prior, alpha=0.5, label="prior", c="orange" )

plt.fill_between( pi_range, prior, alpha=0.3, color="orange" )

# scaled likelihood

likelihood = [stats.binom.pmf(n=n, k=k, p=pi) for pi in pi_range]

likelihood /= np.sum( likelihood ) * (pi_range[1]-pi_range[0])

plt.plot( pi_range, likelihood, alpha=0.5, label="(scaled) likelihood", c="blue" )

plt.fill_between( pi_range, likelihood, alpha=0.3, color="blue" )

# posterior

posterior = [stats.beta.pdf(pi, a=alpha+k, b=beta+n-k) for pi in pi_range]

plt.plot( pi_range, posterior, alpha=0.5, label="posterior", color="darkgreen" )

plt.fill_between( pi_range, posterior, alpha=0.3, color="darkgreen" )

# enable legend and set descriptive title

plt.legend( fontsize=14 )

plt.title( "$\\alpha = {}, \\beta={}, n={}, k={}$".format(alpha, beta, n, k) )

plot_beta_binomial(alpha=5, beta=11, n=20, k=9)

Notebook Cell

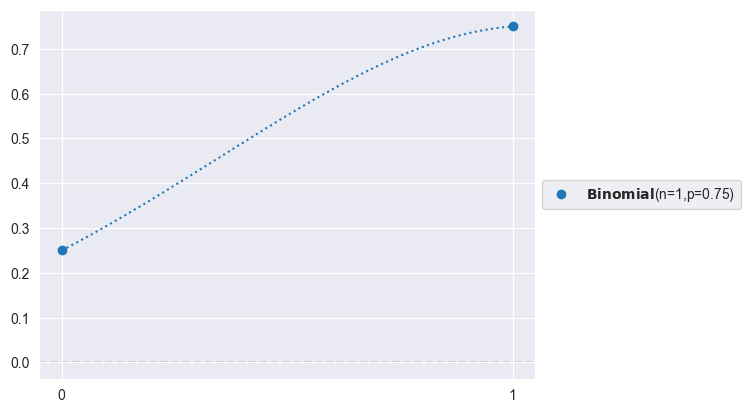

# Likelihood (Binomial counts):

import preliz as pz

pz.Binomial(n=1, p=0.75).plot_pdf()<Axes: >

Notebook Cell

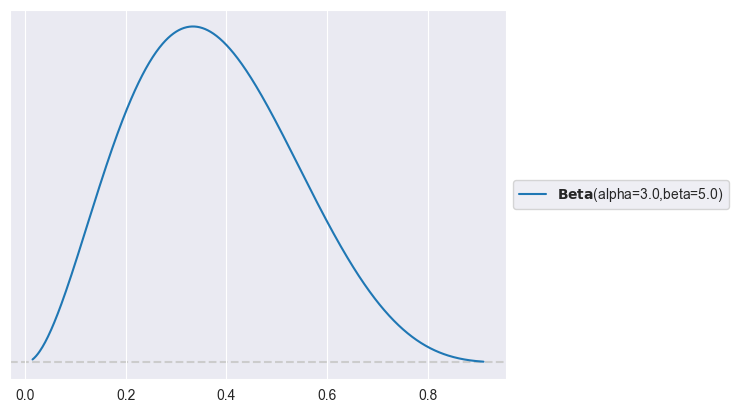

# Prior:

import preliz as pz

pz.Beta(alpha=3, beta=5).plot_pdf()<Axes: >

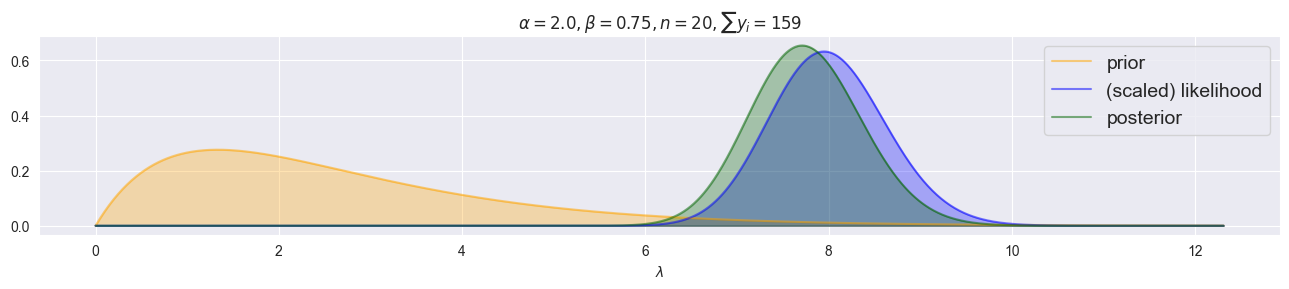

Poisson–Gamma: For Counts¶

Likelihood:

is the contribution from events occurring

is the probability of no other events occurring

normalizes for the ordering of events

Prior:

with

Posterior:

Key properties: Prior “pseudo-counts”: represents prior event count, represents prior observation periods.

With more data, likelihood dominates; with little data, prior dominates.

Order of data does not matter; only sufficient statistic .

Notebook Cell

def plot_gamma_poisson(alpha, beta, y, figsize=(13, 3)):

y = np.asarray(y)

n = len(y)

sum_y = y.sum()

# Posterior hyperparameters

alpha_post = alpha + sum_y

beta_post = beta + n

# Choose a range for lambda using high quantiles of prior and posterior

# (robust and adaptive to parameter scale)

# scipy.stats.gamma uses shape 'a' and scale = 1/rate

scale_prior = 1.0 / beta

scale_post = 1.0 / beta_post

lam_max = max(

stats.gamma.ppf(0.999, a=alpha, scale=scale_prior),

stats.gamma.ppf(0.999, a=alpha_post, scale=scale_post)

)

lam_range = np.linspace(0, lam_max, 1000)

plt.figure(figsize=figsize)

# Prior

prior = stats.gamma.pdf(lam_range, a=alpha, scale=scale_prior)

plt.plot(lam_range, prior, alpha=0.5, label="prior", c="orange")

plt.fill_between(lam_range, prior, alpha=0.3, color="orange")

# Likelihood as function of lambda: L(λ) = ∏_i Pois(y_i | λ)

# Use log-likelihood for numerical stability

log_like = np.zeros_like(lam_range)

for yi in y:

log_like += stats.poisson.logpmf(yi, mu=lam_range)

likelihood = np.exp(log_like)

# Numerically normalize likelihood over lam_range so it behaves like a pdf on this grid

norm_const = np.trapz(likelihood, lam_range)

if norm_const > 0:

likelihood /= norm_const

plt.plot(lam_range, likelihood, alpha=0.5, label="(scaled) likelihood", c="blue")

plt.fill_between(lam_range, likelihood, alpha=0.3, color="blue")

# Posterior

posterior = stats.gamma.pdf(lam_range, a=alpha_post, scale=scale_post)

plt.plot(lam_range, posterior, alpha=0.5, label="posterior", color="darkgreen")

plt.fill_between(lam_range, posterior, alpha=0.3, color="darkgreen")

# Legend and title

plt.legend(fontsize=14)

plt.xlabel(r"$\lambda$")

plt.title(r"$\alpha = {}, \beta = {}, n = {}, \sum y_i = {}$"

.format(alpha, beta, n, int(sum_y)))

plt.tight_layout()

plt.show()

plot_gamma_poisson(alpha=2.0, beta=0.75, y=[7, 8, 3, 7, 11, 7, 9, 19, 7, 15, 9, 5, 12, 3, 7, 6, 5, 3, 11, 5])

Negative Binomial For Overdispersed Counts¶

Unlike the Poisson distribution, the variance is not equal to the mean; it is larger (overdispersion). As the dispersion parameter , the Negative Binomial distribution converges to the Poisson distribution. The Negative Binomial likelihood does not have a simple closed-form conjugate posterior - posterior inference must be done via MCMC simulation.

Likelihood:

probability of success

is the number of successes (-1 because last success is fixed as its the stopping criterion)

is the number of failures

Prior: Negative Binomial is typically used in models where conjugacy does not hold. Therefore, we often use:

in simple models or in regression with

or (must be positive)

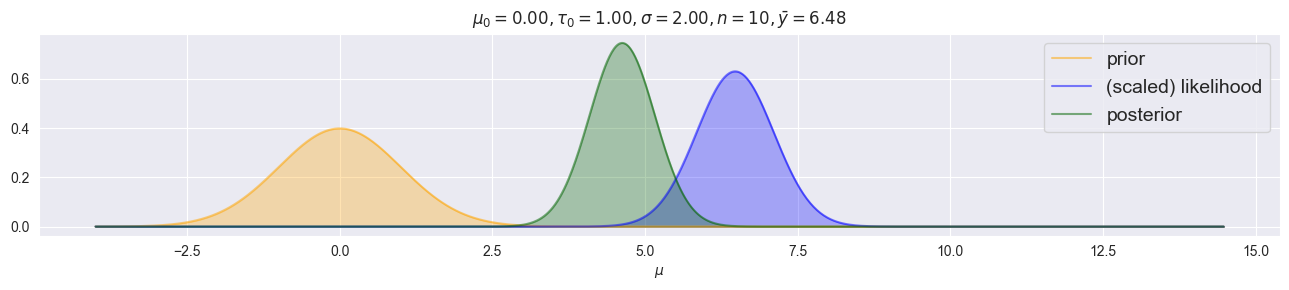

Normal–Normal (variance needs to be known!)¶

Likelihood:

is the mean (location parameter)

is the variance (assumed known)

measures squared deviation from the mean

Prior:

is the prior mean

is the prior variance (reflects uncertainty about )

Posterior:

Key properties: Posterior mean is a precision-weighted average of prior mean and data .

Precision = : higher precision = more influence.

Posterior variance is always smaller than both prior and data variance (information accumulation).

With more data ( observations), data precision dominates.

Notebook Cell

def plot_normal_normal(mu0, tau0, sigma, y, figsize=(13, 3)):

y = np.asarray(y)

n = len(y)

ybar = y.mean()

# Posterior variance and mean

tau_n2 = 1.0 / (n / sigma**2 + 1.0 / tau0**2)

mu_n = tau_n2 * (n * ybar / sigma**2 + mu0 / tau0**2)

tau_n = np.sqrt(tau_n2)

# Choose a plotting range for mu around data and prior

mu_min = min(ybar - 4 * sigma, mu0 - 4 * tau0, mu_n - 4 * tau_n)

mu_max = max(ybar + 4 * sigma, mu0 + 4 * tau0, mu_n + 4 * tau_n)

mu_range = np.linspace(mu_min, mu_max, 1000)

plt.figure(figsize=figsize)

# Prior over mu

prior = stats.norm.pdf(mu_range, loc=mu0, scale=tau0)

plt.plot(mu_range, prior, alpha=0.5, label="prior", c="orange")

plt.fill_between(mu_range, prior, alpha=0.3, color="orange")

# Likelihood as function of mu (up to constant)

# Equivalent to N(mu | ybar, sigma^2/n)

like_unnorm = stats.norm.pdf(mu_range, loc=ybar, scale=sigma / np.sqrt(n))

# Numerically normalize to integrate ~1 on this grid

norm_const = np.trapz(like_unnorm, mu_range)

likelihood = like_unnorm / norm_const if norm_const > 0 else like_unnorm

plt.plot(mu_range, likelihood, alpha=0.5, label="(scaled) likelihood", c="blue")

plt.fill_between(mu_range, likelihood, alpha=0.3, color="blue")

# Posterior over mu

posterior = stats.norm.pdf(mu_range, loc=mu_n, scale=tau_n)

plt.plot(mu_range, posterior, alpha=0.5, label="posterior", color="darkgreen")

plt.fill_between(mu_range, posterior, alpha=0.3, color="darkgreen")

# Legend and title

plt.legend(fontsize=14)

plt.xlabel(r"$\mu$")

plt.title(

r"$\mu_0 = {:.2f}, \tau_0 = {:.2f}, \sigma = {:.2f}, n = {}, \bar y = {:.2f}$"

.format(mu0, tau0, sigma, n, ybar)

)

plt.tight_layout()

plt.show()

np.random.seed(0)

plot_normal_normal(mu0=0.0, tau0=1.0, sigma=2.0, y=np.random.normal(loc=5.0, scale=2.0, size=10))

Multivariate Problems¶

Covariance: Quantifying Relationship Between Variables¶

: A variable’s covariance with itself is its variance

: and are unrelated; on average there is no “co-variance”

For observed data (empirical), the sample covariance is:

and : the sample means

is the number of observations (the denominator is to account for the loss of one degree of freedom when estimating the means)

Pearson Correlation = Standardized Covariance¶

Pearson correlation normalizes covariance by the standard deviations of both variables, producing a unitless measure bounded between 0 and 1. By standardizing covariance, correlation becomes interpretable on a common scale where indicates perfect positive correlation, indicates no correlation, and indicates perfect negative correlation.

and are the standard deviations of and respectively

For observed data (empirical), the Pearson Correlation is:

and are the sample standard deviations

Multinomial–Dirichlet: For Categorical Counts (Generalized Beta-Binomial)¶

Use whenever we want to model experiments with > 2 mutually exclusive outcomes!

Likelihood:

is the contribution from observed category counts

normalizes for the number of orderings

Constraint: and

Prior:

with

Posterior:

Key properties: Prior “pseudo-counts”: represents prior observations in category . Setting (flat prior) means no prior preference.

With more data, likelihood dominates; with little data, prior dominates.

Order of data does not matter; only sufficient statistic .

Conjugate family ensures posterior is also Dirichlet with simple parameter update.

Multivariate Normal¶

, with mean and covariance matrix

Closed under linear transformations, addition, marginalization, conditioning

Covariance controls scale and correlation; must be symmetric and positive definite

LKJ prior for correlation matrices: flexible prior on correlation structures; together with priors on standard deviations gives LKJCov prior for

Multinomial–Dirichlet¶

Likelihood: counts over categories, .

Prior: Dirichlet, .

Posterior: Dirichlet, where counts in category .

Used for compositional data (election results, topic proportions).

Markov Chain Monte Carlo and the Metropolis Algorithm¶

Goal: obtain samples from when no closed form is available. MCMC constructs a Markov chain whose stationary distribution is the posterior.

Metropolis algorithm (random-walk variant)¶

Notebook Cell

from scipy import stats

import seaborn as sns

from tqdm.auto import tqdm

import matplotlib.pyplot as plt

def propose_jump(pi, sigma):

return stats.norm.rvs( loc=pi, scale=sigma )

def decide(pi, pi2, alpha, beta, n, k, debug=False):

# evaluate prior and likelihood

prior1 = stats.beta.pdf( pi, alpha, beta )

prior2 = stats.beta.pdf( pi2, alpha, beta )

likelihood1 = stats.binom.pmf( n=n, k=k, p=pi )

likelihood2 = stats.binom.pmf( n=n, k=k, p=pi2 )

# define alpha

alpha = min(1, prior2/prior1 * likelihood2/likelihood1)

if debug: print("pi = {:.5f}, pi2 = {:.5f}, alpha = {:.5f}".format(pi, pi2, alpha))

# jump decision

p = np.random.rand()

if p<=alpha and 0 < pi2 < 1:

return pi2

else:

return pi

def metropolis_chain(n_steps, alpha, beta, n, k, sigma):

# initialize

pi = np.random.rand()

chain = []

# create chain

for i in tqdm( range( n_steps ) ):

pi2 = propose_jump( pi, sigma )

pi = decide( pi, pi2, alpha, beta, n, k )

chain.append( pi )

return chain

def metropolis( n_chains, n_steps, alpha, beta, n, k, sigma ):

res = [metropolis_chain( n_steps, alpha, beta, n, k, sigma ) for i in range( n_chains)]

return np.array(res).T # to have chains in columns

def trace_plots(sim):

for i in range( sim.shape[1] ):

plt.figure()

plt.plot( sim[:,i] )

plt.title("Chain {}".format(i+1))

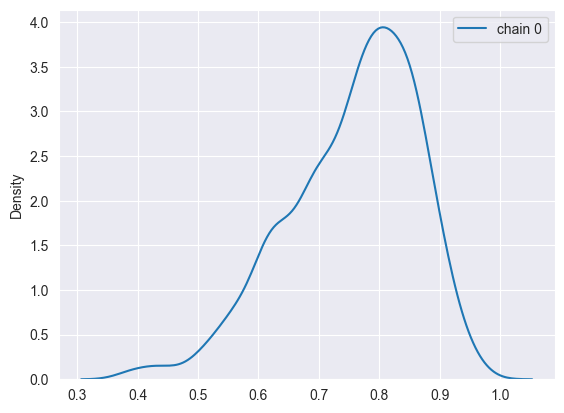

def density_plots( sim ):

plt.figure()

for i in range( sim.shape[1] ):

sns.kdeplot( sim[:,i], label="chain {}".format(i) )

plt.legend()

def rhat( sim ):

total_var = np.var( sim.flatten() )

individual_var = np.var( sim, axis=0 )

rhat = np.sqrt( total_var / np.mean(individual_var) )

return rhat

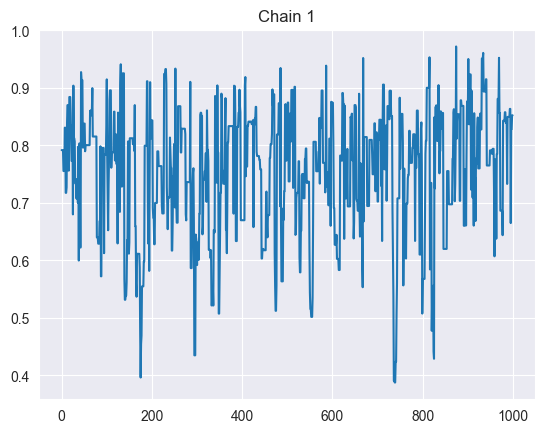

sim = metropolis(n_chains=1, n_steps=1000, alpha=5, beta=2, n=10, k=8, sigma=0.2)

trace_plots(sim)

density_plots(sim)

print(f"Rhat: {rhat(sim)}")Rhat: 1.0

For target density and symmetric proposal distribution , the Metropolis steps are:

Initialize (e.g. some reasonable value).

For iterations :

Propose new state . E.g. random walk: .

Compute acceptance probability

Accept or reject: Draw , If , set (move), Else set (stay).

After burn‑in and thinning, use remaining samples as approximate draws from the posterior.

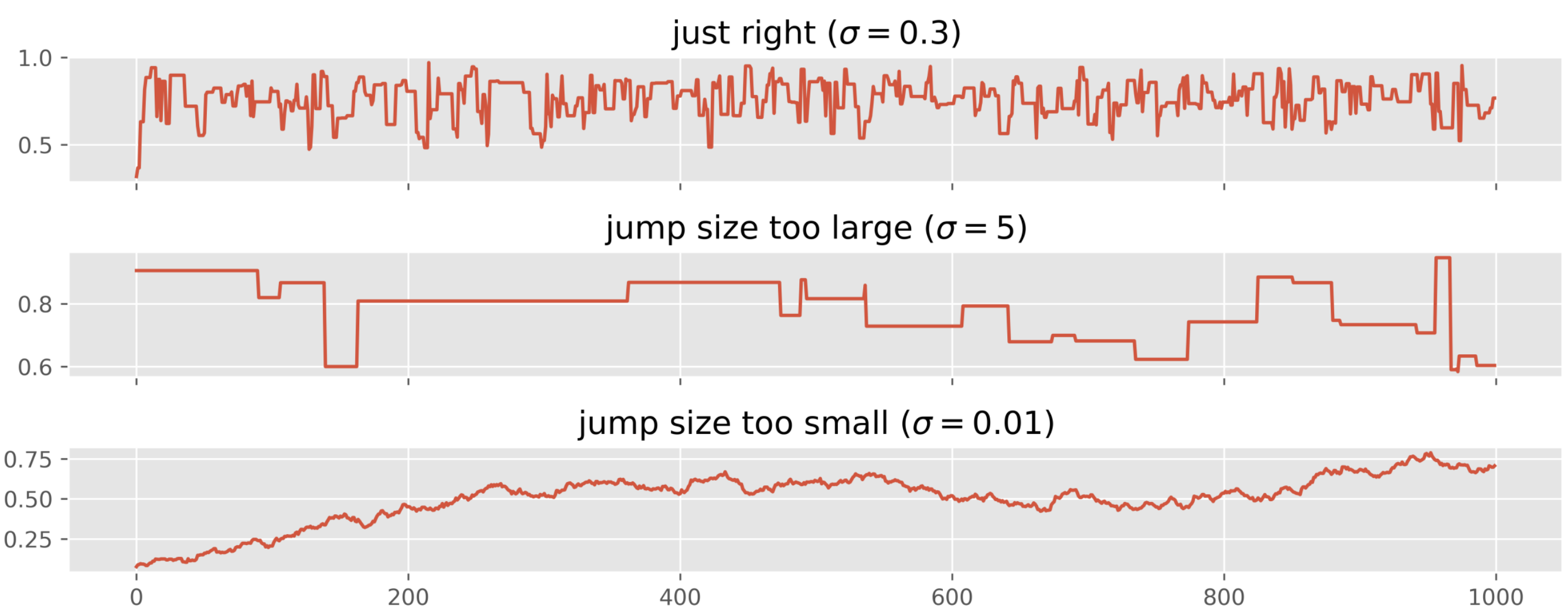

Proposal distribution: the distribution from which proposed new parameters are drawn (). Choice of its scale strongly affects mixing and acceptance rate.

MCMC with PyMC¶

import pymc as pm

# PyMC for Beta-Binominal Conjugate Family

with pm.Model() as beta_binom_model:

pi = pm.Beta("pi", alpha=5, beta=2)

y = pm.Binomial("y", p=pi, n=10, observed=8)

trace = pm.sample(1000)Output

Notebook Cell

import arviz as az

import pandas as pd

def uncertainty_binominal(trace_posterior, var_name: str, n: int, **kwargs):

assert var_name != None, "var_name is required for pi"

assert n != None and n > 0, "n must be > 0"

values = trace_posterior[var_name].values

aleatoric_var = (n * values * (1.0 - values)).mean()

epistemic_var = (values * n).var(ddof=1)

return aleatoric_var, epistemic_var

def uncertainty_normal(trace_posterior, mu: str = "mu", sigma: str = "sigma", **kwargs):

aleatoric_var = (trace_posterior[sigma].values**2).mean()

epistemic_var = trace_posterior[mu].var(ddof=1).values

return aleatoric_var, epistemic_var

def uncertainty_poisson(trace_posterior, var_name: str, n: int, **kwargs):

assert var_name != None, "var_name is required for lambda"

values = trace_posterior[var_name].values

aleatoric_var = values.mean()

epistemic_var = values.var(ddof=1)

return aleatoric_var, epistemic_var

def uncertainty_summary(trace_posterior, family=None, **kwargs):

"""

Computes the aleatoric (data), epistemic (model uncertainty) and predictive (overall uncertainty) variance of a pymc trace.posterior

Parameters

----------

trace_posterior : array_like

Array containing numbers whose mean is desired. If `a` is not an

array, a conversion is attempted.

family : str

Either one of 'binominal', 'normal' or 'poisson'.

For family='binominal':

-----------------------

var_name : str

Name of the Pi variable in the trace_posterior

n : int

Number of trials

For family='normal':

-----------------------

mu : str

Name of the parameter that represents the mean of the normal distribution.

sigma : str

Name of the parameter that represents the standard deviation of the normal distribution.

For family='poisson':

-----------------------

var_name : str

Name of the lambda variable in the trace_posterior

"""

assert trace_posterior != None, "trace_posterior must be provided"

assert family != None, "family must be provided"

uncertainty_stats = pd.DataFrame()

match family:

case 'binominal':

aleatoric_var, epistemic_var = uncertainty_binominal(trace_posterior, **kwargs)

case 'normal':

aleatoric_var, epistemic_var = uncertainty_normal(trace_posterior, **kwargs)

case 'poisson':

aleatoric_var, epistemic_var = uncertainty_poisson(trace_posterior, **kwargs)

case _:

raise ValueError(f"Unknown family: {family}")

predictive_var = aleatoric_var + epistemic_var

uncertainty_stats[family] = {

'var_aleatoric': aleatoric_var,

'var_epistemic': epistemic_var,

'var_predictive': predictive_var,

'var_aleatoric_percent': aleatoric_var / predictive_var,

'var_epistemic_percent': epistemic_var / predictive_var,

}

# switch rows and columns:

uncertainty_stats = uncertainty_stats.T

return uncertainty_stats

def trace_summary(trace, hdi_prob=0.8, var_names=None):

# Use `var_names=['pi', ...]` to limit to vars of interest

stats = az.summary(trace, hdi_prob=hdi_prob, var_names=var_names)

# Variance = standard deviation ** 2:

stats.insert(stats.columns.get_loc('sd') + 1, 'var', stats.sd ** 2)

stats.insert(stats.columns.get_loc('mcse_sd') + 1, 'mcse_var', stats.mcse_sd ** 2)

hdi_alpha = 1.0 - hdi_prob

hdi_low = f'hdi_{100 * hdi_alpha / 2:g}%'

hdi_high = f'hdi_{100 * (1 - hdi_alpha / 2):g}%'

stats.insert(stats.columns.get_loc(hdi_high) + 1, 'hdi_low', stats[hdi_low])

stats.insert(stats.columns.get_loc(hdi_high) + 2, 'hdi_high', stats[hdi_high])

return statsNotebook Cell

import pymc as pm

import arviz as az

# Data: k successes out of n trials

n = 40

k = 26

with pm.Model() as model:

# Prior on probability pi

pi = pm.Beta("pi", alpha=1.0, beta=1.0) # flat prior

# Likelihood

y = pm.Binomial("y", n=n, p=pi, observed=k)

# Sample with NUTS (HMC variant; more efficient than plain Metropolis)

trace = pm.sample(

draws=2000,

tune=1000,

chains=4,

target_accept=0.9,

random_seed=42

)Diagnosing convergence and mixing¶

Key visual and numeric diagnostics:

Trace plots: Plot each chain’s sampled values over iterations

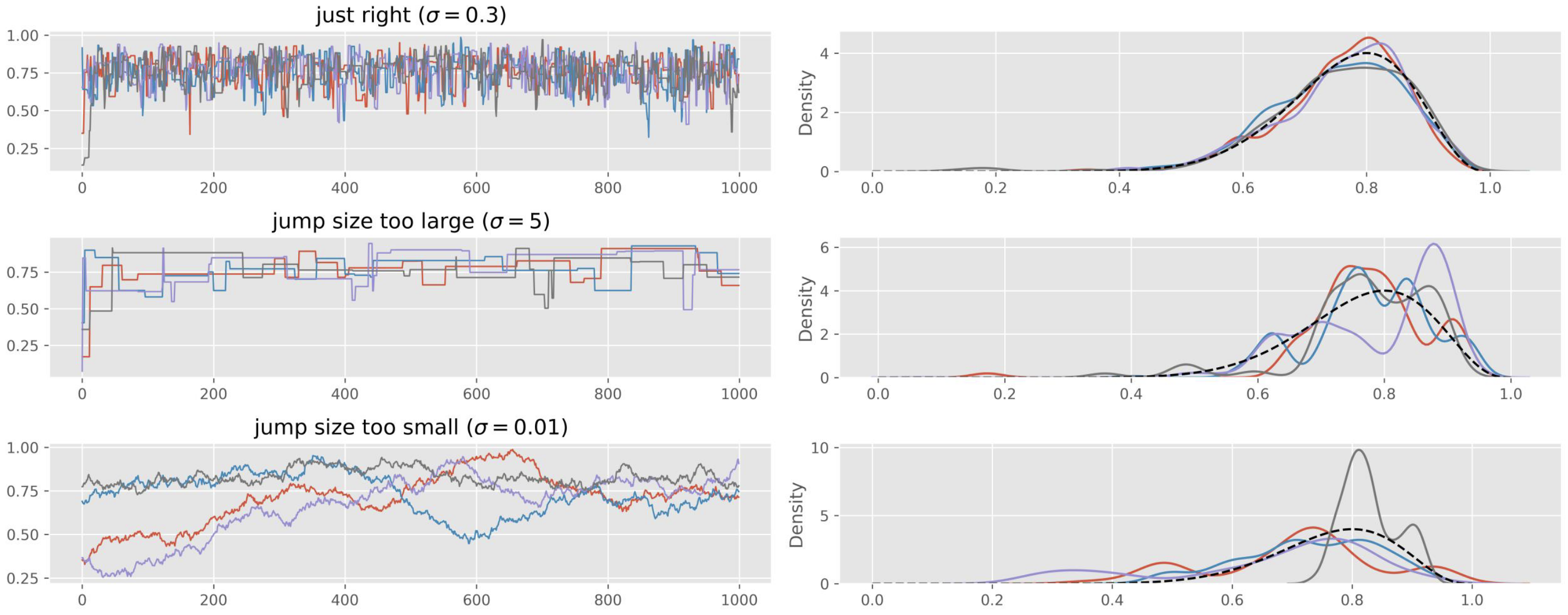

For Metropolis specifically, problematic trace plots often indicate: Proposal variance too small (tiny steps, high acceptance, poor exploration). Proposal variance too large (proposals rejected, chain rarely moves). Tunable by adjusting .

Notebook Cell

import arviz as az

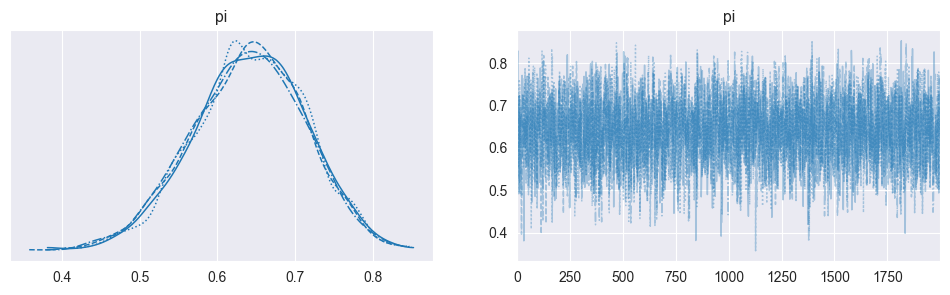

az.plot_trace(trace, kind='trace', figsize=(12, 3))

plt.show()

Chains explore the same region (“fuzzy caterpillars”)

No systematic upward or downward drift.

No chains stuck in a narrow band.

Different chains overlap well.

Run multiple chains: Posterior histograms or kernel density estimates for each chain separately

Distributions from all chains almost perfectly overlap.

No unique behavior in one chain.

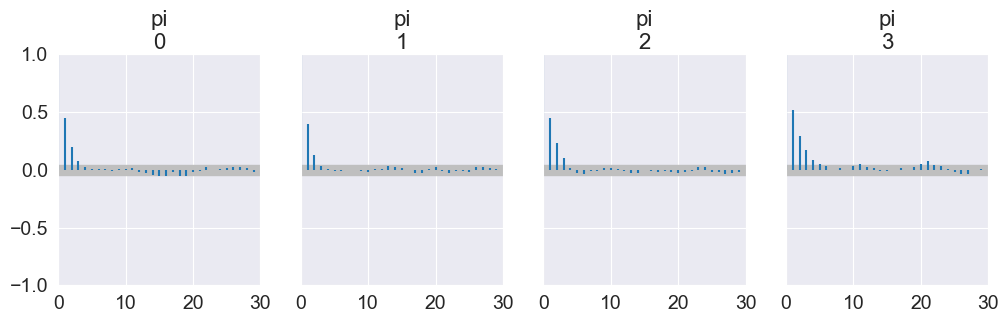

Autocorrelation plots: Autocorrelation function (ACF) of each chain as a function of lag

Source

import arviz as az

import matplotlib.pyplot as plt

az.plot_autocorr(trace, max_lag=30, figsize=(12, 3))

plt.show()

Autocorrelation decays quickly with lag.

Very slow decay or persistent high correlation means poor mixing and low effective sample size.

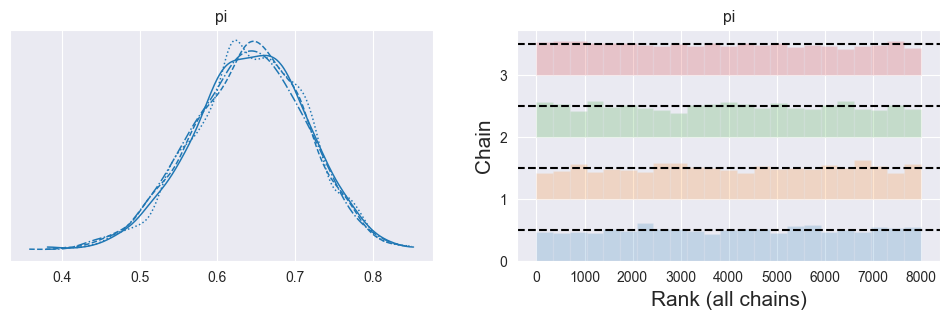

Rank plots / rank bars: For each parameter, pool all samples from all chains, compute their ranks, then see how ranks are distributed per chain (as in ArviZ’s rank plots)

Source

import arviz as az

import matplotlib.pyplot as plt

az.plot_trace(trace, kind='rank_bars', figsize=(12, 3))

plt.show()

Ranks within each chain are roughly uniformly distributed.

All chains show similar, flat-ish rank patterns.

Strong deviations (U‑shape, spikes, or clearly different patterns per chain) indicate non‑convergence or poor mixing.

(R‑hat, Gelman–Rubin statistic): Compares total chain data variance (concatenated) vs. the mean variance within individual chains. Summarizes the overlaid density plots of multiple chains and provides a numerical measure for their diagreement.

Notebook Cell

trace_summary(trace)(e.g. < 1.01–1.05) means chains have likely converged to same target distribution.

means potential non‑convergence; increase iterations, needs better initialization, or reparameterization.

ESS (effective sample size): Estimates how many independent draws your autocorrelated chain is equivalent to

Notebook Cell

trace_summary(trace)ESS large relative to the number of draws, giving stable posterior summaries. Rule of thumb: ESS / N > 10%

Very small ESS (especially compared to total draws) means strong autocorrelation, poor mixing, unreliable summaries.

ess_bulk (Bulk ESS): Use this to assess reliability of posterior means, medians, and central credible intervals. Estimates the effective sample size for the central part of the distribution (around the median/mean). Interpretation: Higher is better. If ess_bulk is very small relative to the total number of draws, the chain is autocorrelated or has poor mixing in the center of the distribution.

ess_tail (Tail ESS): Use this to assess reliability of HDI/credible interval bounds and tail probabilities. Estimates the effective sample size specifically for the tails of the distribution (extreme quantiles, typically 5th and 95th percentiles). Interpretation: Higher is better. Can be substantially lower than ess_bulk if the tails are poorly explored.

Posterior Summaries, Prediction, and Uncertainty¶

Notebook Cell

import pymc as pm

import arviz as az

# Data: k successes out of n trials

n = 40

k = 26

with pm.Model() as model:

pi = pm.Beta("pi", alpha=1.0, beta=1.0) # Prior on probability pi

y = pm.Binomial("y", n=n, p=pi, observed=k) # Likelihood

trace = pm.sample( # Sample posterior

draws=2000,

tune=1000,

chains=4,

target_accept=0.9,

random_seed=42

)

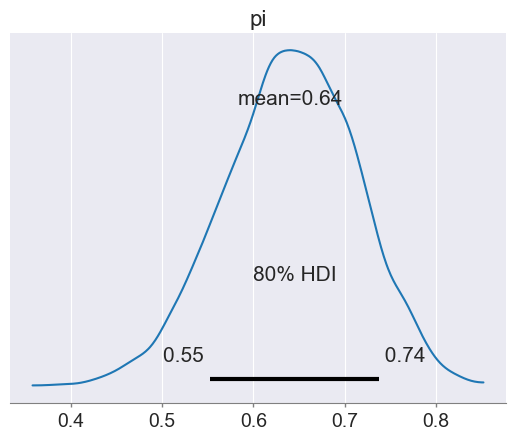

az.plot_posterior(trace, hdi_prob=0.80) # Posterior plot: shows density + HDI interval + mean

trace_summary(trace, hdi_prob=0.80)

Point Summaries: Mean, Variance, Maximum A Posteriori (MAP / Posterior Mode)¶

Notebook Cell

stats = trace_summary(trace)

stats # Use `stats.loc['pi']['mean']` to access specific valuesGiven posterior samples :

Posterior mean:

Posterior variance:

Maximum A Posteriori (MAP) or Posterior Mode: ; To compute: Use closed form Posterior Mode if available; or Differentiate with respect to , set the derivative to zero, and solve for ; or use numerical optimization when there is no closed form.

Credible Intervals vs. Confidence Intervals¶

Source

import numpy as np

import pymc as pm

import matplotlib.pyplot as plt

from scipy.stats import beta

from statsmodels.stats.proportion import proportion_confint

pi_x = np.linspace(0, 1, 500)

# Data: k successes out of n trials

n = 40

k = 26

p_hat = k / n

# Prior parameters: Beta(1,1) -> flat

alpha_prior = 1.0

beta_prior = 1.0

# Posterior parameters

alpha_posterior = alpha_prior + k

beta_posterior = beta_prior + n - k

pi_y = beta.pdf(pi_x, a=alpha_posterior, b=beta_posterior)

with pm.Model() as model_binom:

pi = pm.Beta("pi", alpha=alpha_prior, beta=beta_prior) # Prior on probability pi

y = pm.Binomial("y", n=n, p=pi, observed=k) # Likelihood

trace = pm.sample( # Sample posterior

draws=2000,

tune=1000,

chains=4,

target_accept=0.9,

random_seed=42

)

stats = trace_summary(trace, hdi_prob=0.95, var_names=['pi'])

ci_low, ci_high = proportion_confint(k, n, alpha=0.05)

# print(f"Posterior mean (pi) = {stats.loc['pi']['mean']:.4f}")

# print(f"Bayesian credible interval (HDI) = {[stats.loc['pi']['hdi_low'], stats.loc['pi']['hdi_high']]}")

# print(f"Frequentist confidence interval (CI) = {[ci_low, ci_high]}")

plt.figure(figsize=(7, 4))

# Posterior density

def plot_density(x, y, label, color='darkgreen'):

plt.plot(x, y, label=label, lw=2, color=color)

plt.fill_between(x, y, alpha=0.2, color=color)

plot_density(pi_x, pi_y, label="Posterior density")

# Shade Bayesian credible interval (HDI)

plt.axvspan(stats.loc['pi']['hdi_low'], stats.loc['pi']['hdi_high'], color="green", alpha=0.2, label="Bayesian credible interval (HDI)")

# Mark frequentist CI as a horizontal bar at y=0

plt.hlines(y=0.0,xmin=ci_low,xmax=ci_high,colors="red",linewidth=4,label="Frequentist confidence interval (CI)")

# Mark posterior mean and p_hat

plt.axvline(stats.loc['pi']['mean'], color="k", linestyle="--", label="Posterior mean")

plt.axvline(p_hat, color="blue", linestyle="--", label="Sample proportion $\hat p$")

plt.xlim(0, 1)

plt.xlabel(r"$\pi$")

plt.ylabel("density")

plt.title("Posterior density with Bayesian credible interval vs frequentist CI")

plt.legend(loc="upper left", fontsize=9)

plt.tight_layout()

plt.show()

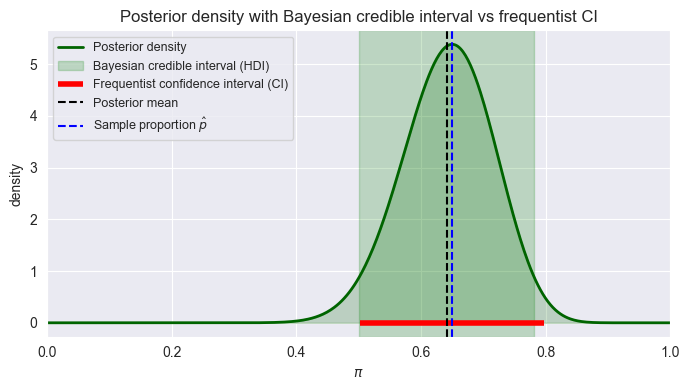

Credible interval (Bayesian): For posterior , an 80% credible interval satisfies: . It’s a direct statement about the parameter: “Given data and model, we believe with 80% plausibility that lies in .”

HDI (Highest Density Interval): Among all 80% intervals, choose the one where posterior density is everywhere at least as high as outside. It minimizes width for a given mass; It contains the most probable values by construction.

Confidence interval (frequentist): 80% CI: in 80% of repeated experiments, the interval constructed by a given procedure will contain the fixed true . It does not allow the statement “ is in this specific interval with probability 0.8”.

Aleatoric vs. Epistemic Uncertainty¶

Law of total variance:

Aleatoric Uncertainty: irreducible data noise (e.g. binomial or Gaussian observation noise).

Epistemic Uncertainty: uncertainty about model parameters; reducible with more/better data.

If Epistemic is bigger than Aleatoric, it means collecting more data can meaningfully reduce predictive uncertainty.

If Aleatoric is bigger than Epistemic, it means that even infinite data cannot substantially reduce predictive spread (inherent randomness).

Notebook Cell

uncertainty_summary(trace.posterior, family='binominal', n=n, var_name='pi')

# uncertainty_summary(trace.posterior, family='normal', mu='mu', sigma='sigma')

# uncertainty_summary(trace.posterior, family='poisson', var_name='lambda')Notebook Cell

# Double check with posterior predictive:

var_name = 'y'

with model:

predictions = pm.sample_posterior_predictive(trace, var_names=[var_name], random_seed=42)

predictive_var = predictions.posterior_predictive[var_name].var(ddof=1).values

print(f"Predictive Variance = {predictive_var} (for {predictions.posterior_predictive.y.values.size} samples)")

trace_summary(predictions.posterior_predictive, var_names=[var_name])Predictive Variance = 17.244173631078883 (for 8000 samples)

Hypothesis Testing¶

Many branches of science depend on hypothesis testing to build knowledge. Hypothesis tests are often used for feature selection (e.g. t-test p-value for features in frequentist linear regression). In Bayesian statistics, one method for model selection is based on hypothesis testing (a model is a hypothesis).

Frequentist vs. Bayesian Hypothesis Tests¶

Frequentist hypothesis testing can only compute the probability of data under a given hypothesis. Set up a null hypothesis and discard it if the probability is too low. This approach is dangerous when we measure unlikely data or are looking at unlikely hypotheses.

Bayesian hypothesis testing can compute , i.e. our posterior belief in given data ! Does not need a null hypothesis - can compare any two or more competing hypotheses! Bayesian and frequentist hypothesis tests return different results whenever there is heavy prior belief in and we have measured unlikely data that are in favor of : The Bayesian approach is more robust in this case because it supports the philosophy of “one random accident should not overthrow an established theory”.

One-Sided Hypothesis Tests¶

Frequentist Hypothesis Test: Null Hypothesis Significance Testing (NHST)

Define and

Define an estimator and significance level (false positive rate, usually )

Define a test statistic (i.e. z-score in case of binominal distribution, type of test statistic depends on estimator!):

Determine p-value:

If , reject $

Bayesian Hypothesis Test: Compare posterior probability of hypotheses

Define and :

80% of people or less in the local population are able to roll their tongue

More than 80% of people in the local population are able to roll their tongue

Define a prior distribution for (e.g. Beta(1,1) for flat prior)

Define a likelihood function (e.g. Binomial likelihood)

Sample posterior

Approximate posterior distribution of using and

pH1d = np.mean(trace.posterior.pi.values > 0.8)

pH1d, 1.0 - pH1dNotebook Cell

# With posterior samples pi_i, approximate:

import numpy as np

import pymc as pm

# Data: k successes out of n trials

n = 40

k = 26

with pm.Model() as one_sided_model:

# Prior on pi: flat Beta(1,1)

pi = pm.Beta("pi", alpha=1.0, beta=1.0)

# Likelihood

y = pm.Binomial("y", n=n, p=pi, observed=k)

# Sample posterior

trace = pm.sample(

draws=3000,

tune=1000,

chains=4,

target_accept=0.9,

random_seed=42

)

# Extract posterior samplesd

pi_samples = trace.posterior["pi"].values.flatten()

# Posterior probability of H1: pi > 0.8

P_H1_post = np.mean(pi_samples > 0.8)

P_H0_post = 1.0 - P_H1_post

print(f"P(H1: pi > 0.8 | data) = {P_H1_post:.3f}")

print(f"P(H0: pi ≤ 0.8 | data) = {P_H0_post:.3f}")

print(f"Posterior odds H1:H0 = {P_H1_post / P_H0_post:.3f}")P(H1: pi > 0.8 | data) = 0.010

P(H0: pi ≤ 0.8 | data) = 0.990

Posterior odds H1:H0 = 0.010

Bayes Factor and Odds¶

Notebook Cell

# Prior probabilities under Beta(1,1)

P_H0_prior = 0.8

P_H1_prior = 1.0 - P_H0_prior # P(pi > 0.8) for uniform prior = 0.2

prior_odds = P_H1_prior / P_H0_prior

post_odds = P_H1_post / P_H0_post

BF_10 = post_odds / prior_odds

print(f"Prior Odds H1:H0 = {prior_odds:.3f}")

print(f"Posterior Odds H1:H0 = {post_odds:.3f}")

print(f"Bayes Factor BF_10 = {BF_10:.3f}")Prior Odds H1:H0 = 0.250

Posterior Odds H1:H0 = 0.010

Bayes Factor BF_10 = 0.040

Prior odds for vs (how much more likely is than ): , flip the ratio if you are interested in how much more likely is than

Posterior odds after data:

Bayes factor , describes how much my believe changed or how much I learned from the data. Rules of Thumb: 1–3: barely worth mentioning, 3–10: substantial, 10–100: strong, bigger than 100: decisive evidence in favour of .

Two-Sided Hypothesis Tests¶

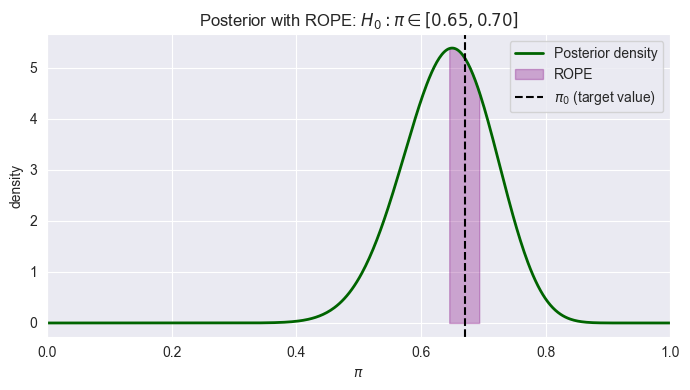

Region of Practical Equivalence (ROPE)¶

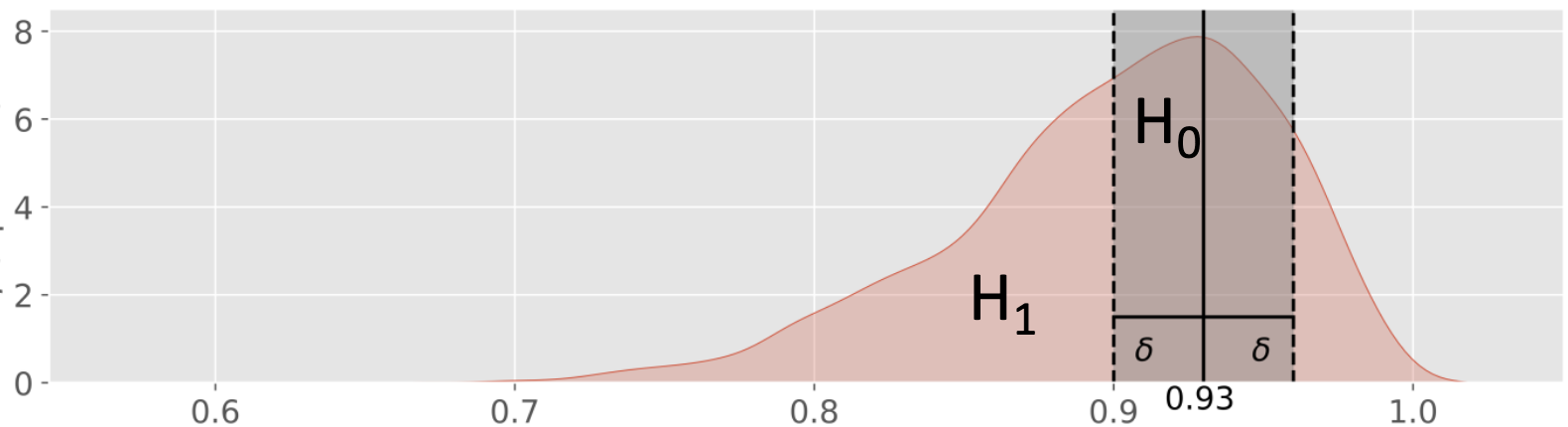

In Bayesian inference, testing whether a parameter exactly equals a specific value is statistically problematic because the probability of a continuous parameter equaling any single point is essentially zero. Instead, ROPE defines a range of values considered “practically equivalent” to the null hypothesis. For testing whether a parameter is practically equal to some value , define a ROPE, e.g. .

: Exactly 93% of people in the local population are able to roll their tongue for and some .

: More or less than 93% of people in the local population are able to roll their tongue outside that interval.

pi0 = 0.93; delta = 0.03

pi_values = trace.posterior.pi.values

pH0d = np.mean((pi_values > pi0 - delta) &

(pi_values < pi0 + delta))

pH1d = 1 - pH0d

pH0d, pH1d, (pH0d / pH1d)If most posterior mass lies inside the ROPE, you accept practical equivalence; otherwise, you conclude a meaningful difference. If the posterior distribution is fairly diffuse, with substantial mass both inside and outside this range a narrow ROPE {small ) can create an inconclusive result. A larger ROPE (bigger ) reflects what differences you actually care about practically: If you only need to know whether the true proportion is “around 93%” rather than “exactly 93%”, a wider ROPE makes sense.

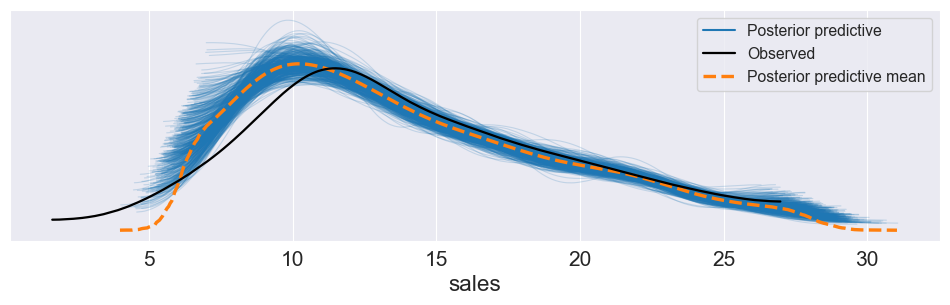

Posterior Predictive Checks¶

Fit model and obtain posterior samples.

For each posterior draw, simulate an entire replicated dataset from the model (posterior predictive).

Compare distribution of replicated data to observed data (histograms, kernel density plots, summary statistics).

If simulated data systematically differ (e.g. lower variance, wrong tail behaviour), the model is likely misspecified (e.g. wrong likelihood family).

Source

import bambi as bmb

import pandas as pd

import numpy as np

import arviz as az

import matplotlib.pyplot as plt

data = pd.read_csv("bayesian-machine-learning/advertising.csv")

model = bmb.Model( "sales ~ TV + radio + TV:radio", data=data, family="gaussian" )

trace = model.fit(draws=2000, tune=2000, chains=4, target_accept=0.9, random_seed=42)

model.predict(trace, kind="pps")

az.plot_ppc(trace, num_pp_samples=500, figsize=(12, 3))

plt.show()

Notebook Cell

import numpy as np

import pymc as pm

# Data: k successes out of n trials

n = 40

k = 26

alpha_prior, beta_prior = 1.0, 1.0

with pm.Model() as one_sided_model:

# Prior on pi: flat Beta(1,1)

pi = pm.Beta("pi", alpha=alpha_prior, beta=beta_prior)

# Likelihood

y = pm.Binomial("y", n=n, p=pi, observed=k)

# Sample posterior

trace = pm.sample(

draws=3000,

tune=1000,

chains=4,

target_accept=0.9,

random_seed=42

)

# Extract posterior samplesd

pi_samples = trace.posterior["pi"].values.flatten()

###################################################

# Compute posterior mass in ROPE and posterior odds

###################################################

# Define ROPE

pi0 = 0.67

delta = 0.025

rope_low = pi0 - delta

rope_high = pi0 + delta

# Posterior probabilities

P_H0_rope = np.mean((pi_samples >= rope_low) & (pi_samples <= rope_high))

P_H1_rope = 1.0 - P_H0_rope

print(f"ROPE = [{rope_low:.2f}, {rope_high:.2f}]")

print(f"P(H0: pi in ROPE | data) = {P_H0_rope:.3f}")

print(f"P(H1: pi outside ROPE | data) = {P_H1_rope:.3f}")

print(f"Posterior odds H0:H1 = {P_H0_rope / P_H1_rope:.3f}")

#######################################

# Visualize posterior with ROPE shaded

#######################################

from scipy.stats import beta

alpha_posterior, beta_posterior = alpha_prior + k, beta_prior + n - k

pi_grid = np.linspace(0, 1, 500)

post_pdf = beta.pdf(pi_grid, a=alpha_posterior, b=beta_posterior)

plt.figure(figsize=(7, 4))

# Posterior density

plt.plot(pi_grid, post_pdf, color="darkgreen", lw=2, label="Posterior density")

# Shade ROPE region

mask_rope = (pi_grid >= rope_low) & (pi_grid <= rope_high)

plt.fill_between(pi_grid[mask_rope], post_pdf[mask_rope], color="purple", alpha=0.3, label="ROPE")

# Vertical line at pi0

plt.axvline(pi0, color="k", linestyle="--", label=r"$\pi_0$ (target value)")

plt.xlabel(r"$\pi$")

plt.ylabel("density")

plt.xlim(0, 1)

plt.title(r"Posterior with ROPE: $H_0: \pi \in [{:.2f}, {:.2f}]$".format(rope_low, rope_high))

plt.legend()

plt.tight_layout()

plt.show()ROPE = [0.65, 0.70]

P(H0: pi in ROPE | data) = 0.245

P(H1: pi outside ROPE | data) = 0.755

Posterior odds H0:H1 = 0.324

Model Checking, Selection, and Multivariate Distributions¶

Model selection criteria¶

The Fully Bayesian way: Use Bayes Factor (based on marginal likelihood). This is conceptually clean, but marginal likelihood can be hard to compute.

Use Predictive Criteria instead: These criteria trade off fit vs complexity; Bayesian evidence automatically penalizes overly complex models (“built-in Occam’s razor”).

RMSE, MAE (point prediction error using posterior predictive means)

ELPD / LOO (Expected Log Predictive Density with leave-one-out cross-validation, Computed with PSIS-LOO, higher is better)

Bayesian for regression

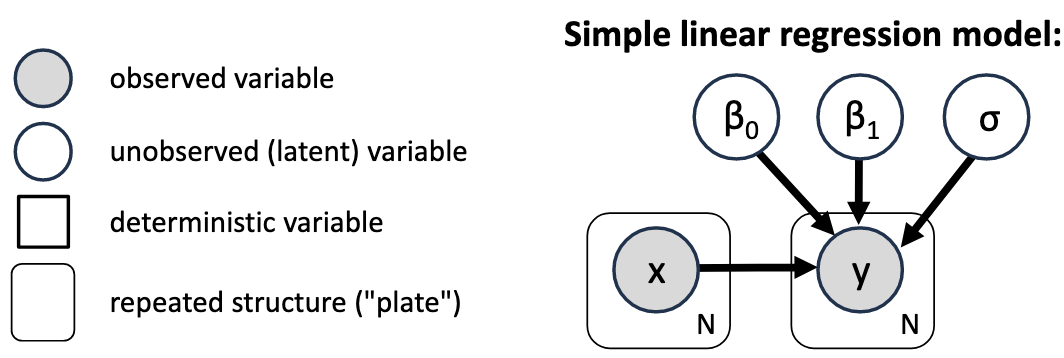

Bayesian Linear Regression¶

What is the posterior distribution of the linear regression parameters , , and ? Use Bayes’ theorem (and condition on ):

Likelihood: — probability of observing the data given parameters

Prior: — treat parameters as independent, no direct dependence on

Evidence: — marginal likelihood computed via MCMC

Then define priors and likelihood distributions:

Probabilistic Graphical Model Notation¶

Compact graphical way to describe a model without the distributions of the individual variables. Every unobserved variable that has no arrows going into it does need a prior. Bayesian inference will get us probability distributions for the unobserved variables.

Implementation and interpretation (PyMC/Bambi)¶

Built-in Bambi Operators

Notebook Cell

import bambi as bmb

import pandas as pd

import arviz as azNotebook Cell

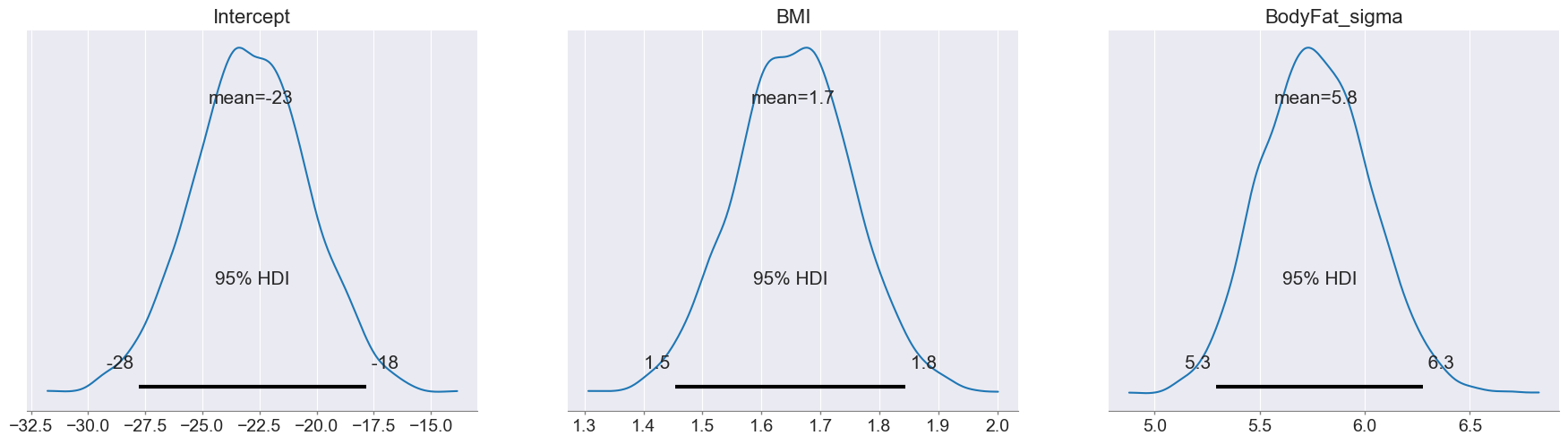

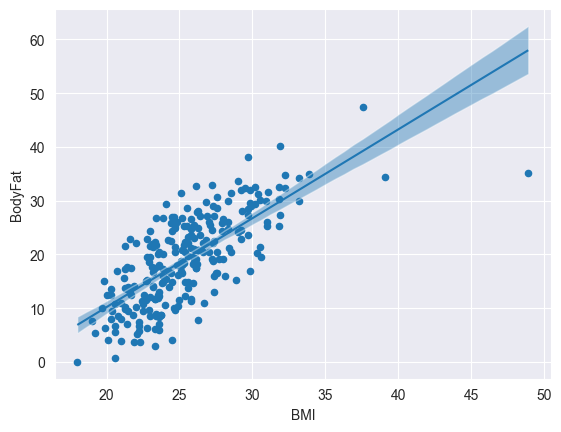

data = pd.read_csv("bayesian-machine-learning/bodyfat.csv")

model = bmb.Model("BodyFat ~ 1 + BMI",

data=data, family="gaussian")

trace = model.fit(draws=1000, tune=1000)

trace_summary(trace, hdi_prob=0.95)Notebook Cell

az.plot_posterior(trace, hdi_prob=0.95)

plt.show()

Notebook Cell

data.plot.scatter(x='BMI', y='BodyFat')

bmb.interpret.plot_predictions(

model, trace, 'BMI', ax=plt.gca())

plt.show()

Notebook Cell

# predict out-of-sample data. for in-sample remove `data=...`

predictions = model.predict(trace, data=pd.DataFrame({ 'BMI': [20, 30, 50] }), kind="pps", inplace=False)

uncertainty_summary(predictions.posterior, family='normal', mu='BodyFat_mean', sigma='BodyFat_sigma')Notebook Cell

predictions.posterior_predictive.BodyFat.var().values # double check posterior predictive variancearray(463.07425281)Robust Linear Regression¶

Motivation: Outliers can have a big impact on the resulting regression line.

Reason: The Gaussian likelihood does not like points far away from its center.

Solution: Can be mitigated using a Student’s t-distribution with a heavier tail. Bayesians often prefer to change the likelihood instead of the data because its more reproducible.

model_robust = bmb.Model("BodyFat ~ BMI",

data=data, family="t")

trace_robust = model.fit(draws=1000, tune=1000)

trace_summary(trace_robust, hdi_prob=0.95)Output

Gaussian Processes (GPs)¶

Intuition and definition¶

Gaussian Processes are prior distributions over functions: . A Gaussian Process is fully characterized by: Mean and a Covariance function

Covariance function must be: Symmetric and Positive semi-definite: for any finite set of inputs, the matrix must produce non-negative quadratic forms . If using a “kernel” that is not positive semi-definite (e.g. ), you can obtain negative predictive variances in the formula . Such a function is not a valid covariance function, because a covariance matrix must be positive semi-definite, implying predictive variance must be .

Key Intuition about Gaussian Processes: If things are close to each other, they should behave similar (i.e. be stronger correlated). That implies that the covariance between outputs is given in terms of the inputs.

Conditioning Rule: (“whats the prediction given the training data”)

Posterior Distribution for given , including observation noise:

Inverting the covariance matrix of the noisy observations is the most computationally expensive step, resulting in a complexity of . Therefore, large datasets are challenging for standard GPs.

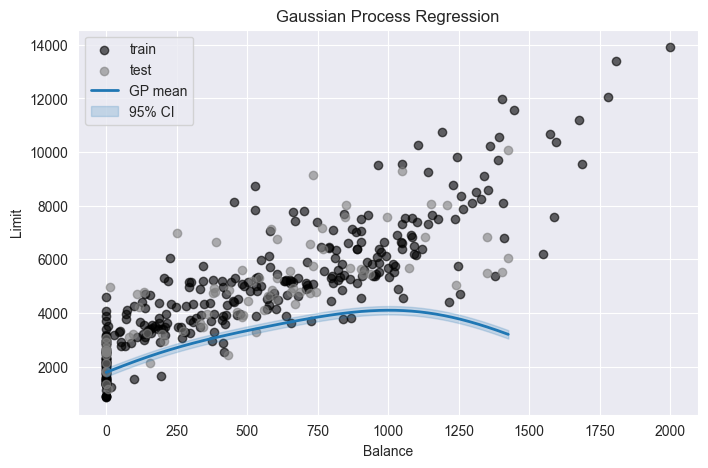

GP regression: predictive mean and variance¶

Notebook Cell

import pandas as pd

import matplotlib.pyplot as plt

from sklearn.gaussian_process.kernels import RBF, WhiteKernel

from sklearn.gaussian_process import GaussianProcessRegressor

from sklearn.model_selection import train_test_split

length_scale = 300.0

variance = 100.0

sigma_obs = 80 # observation noise std

df = pd.read_csv("bayesian-machine-learning/credit_data.csv")

X_train, X_test, y_train, y_test = train_test_split(

df[['Balance']],

df[['Limit']],

test_size=0.2, # 20% test, 80% train

random_state=42, # for reproducibility

shuffle=True # default; set False if time series

)

kernel = variance * RBF(length_scale=length_scale) + WhiteKernel(noise_level=sigma_obs**2)

gpr = GaussianProcessRegressor(kernel=kernel, alpha=0.0, optimizer=None, normalize_y=False)

gpr.fit(X_train, y_train)

X_plot = np.linspace(X_test["Balance"].min(), X_test["Balance"].max(), 400).reshape(-1, 1)

y_mean, y_std = gpr.predict(X_plot, return_std=True)

# ---- Plot ----

plt.figure(figsize=(8, 5))

# Training and test points

plt.scatter(X_train["Balance"], y_train, color="k", alpha=0.6, label="train")

plt.scatter(X_test["Balance"], y_test, color="gray", alpha=0.6, label="test")

# GP mean and 95% interval

plt.plot(X_plot[:, 0], y_mean, color="C0", lw=2, label="GP mean")

plt.fill_between(

X_plot[:, 0],

y_mean - 1.96 * y_std,

y_mean + 1.96 * y_std,

color="C0",

alpha=0.2,

label="95% CI"

)

plt.xlabel("Balance")

plt.ylabel("Limit")

plt.title("Gaussian Process Regression")

plt.legend()

Predictive distribution for response :

Training outputs .

Covariance matrix for training outputs (including noise):

Covariances between test point and training points:

Prior variance at test point (for ):

Connection to kernels and PSD requirement¶

Common kernels and hyperparameters:

Squared Exponential / RBF: , (: output variance, : length scale (smoothness))

Matérn (controls differentiability via ):

Rational Quadratic (mixture over length scales).

Bayesian Networks and Causal Inference¶

Structural Causal Models (SCMs) and Bayesian Networks¶

SCM formalism (from BN lecture notes):

Endogenous (ovservered) variables : determined by structural equations.

Exogenous (unobserved) variables : external noise.

Structural equations: each variable is a function of its parents (endogenous causes) and noise (exogenous causes):

Joint distribution defined via and structural equations.

A Bayesian Network (BN) is a DAG over variables such that joint distribution factorizes as:

Graph encodes conditional independencies.

Each node has a Conditional Probability Table (CPT) or parameterized distribution.

Basic graph motifs and conditional independence¶

Three canonical patterns:

Chain (serial):

and correlated marginally.

Conditional independence given the middle node: .

Fork (common cause):

and correlated marginally (through common cause ).

Conditional independence given cause: .

Collider (v‑structure):

and independent marginally.

Conditioning on collider (or its descendants) induces dependence (explaining away).

Explaining away: In collider , observing the effect makes causes and compete.

Example: “Smoker” and “Covid” both cause “Hospitalization”; given hospitalization, learning that patient is a smoker reduces belief that Covid is cause, and vice versa.

Computing Probabilities from Joint Tables¶

Given full joint distribution table :

Marginal:

Conditional:

Example:

Interventions and the do‑operator¶

Conditioning: describes correlations in observed data; may itself be caused by other variables (confounded).

Intervention: describes what happens if we force to (surgery on the graph):

All incoming edges into are cut.

is set externally.

The rest of the graph and conditional distributions remain unchanged.

For a treatment , outcome , and set of observed confounders that block all backdoor paths (backdoor criterion), adjustment formula:

Expectation Maximization (EM)¶

The EM algorithm iteratively maximizes the log-likelihood of the observed data. is hidden, is observed.

Initialize randomly

Repeat until convergence:

E-step:

Compute for each (probabilistic inference)

Create fully-observed weighted examples: with weight

M-step:

Perform maximum likelihood (count and normalize) on weighted examples to update