Advanced Statistical Data Analysis

Notebook Cell

# Install and load required packages

install.packages("boot")

install.packages("car")

install.packages("MASS")

install.packages("mgcv")

install.packages("splines")

install.packages("gRbase")

install.packages("gRain")

install.packages("pcalg")

install.packages("AER")

library(DAAG)

library(boot)

library(car)

library(MASS)

library(mgcv)

library(splines)

library(gRbase)

library(gRain)

library(pcalg)

library(AER)

# Load custom datasets from advanced-statistical-data-analysis/ folder

# Challenger O-ring data

chal <- read.table("advanced-statistical-data-analysis/O-rings.dat", header = TRUE)

# Dial-a-Ride calls data

dial <- read.table("advanced-statistical-data-analysis/Dial-a-ride.dat", header = TRUE)

# Promotion data

load("advanced-statistical-data-analysis/promotion.rda")

# Source custom functions

source("advanced-statistical-data-analysis/RFn_Plot-glmSim.R")

# Load built-in datasets

library(datasets)

data(mtcars)

data(warpbreaks)

set.seed(42)

FF <- data.frame(

FoodCon = runif(20, 3, 7),

lMaxWt = runif(20, 5, 7.5),

Temp = sample(c(13, 17, 23), 20, replace = TRUE),

lAR = runif(20, -0.5, 0.8),

Food = factor(sample(c("C", "H"), 20, replace = TRUE))

)

# dial can be simulated with:

dial <- data.frame(

Calls = sample(10:20, 10),

Center = factor(rep(c("A", "B"), each = 5)),

Time = 1:10

)

ship <- data.frame(

Damages = c(0, 0, 1, 0, 0, 1, 0, 0, 0, 0, 1, 0, 1, 0, 0, 0, 0, 0, 0, 0),

Year = factor(rep(c("60", "65", "70", "75"), each = 5)), # 4 levels × 5 = 20

Month = factor(rep(c("60", "75"), each = 10)), # 2 levels × 10 = 20

Exposure = c(43, 45, 47, 61, 64, 65, 67, 71, 74, 77, 77, 79, 80, 81, 82, 85, 86, 87, 88, 90)

)

The downloaded binary packages are in

/var/folders/mg/f7gk10vj1_153rz1zkvd13_00000gn/T//RtmpprnLpL/downloaded_packages

The downloaded binary packages are in

/var/folders/mg/f7gk10vj1_153rz1zkvd13_00000gn/T//RtmpprnLpL/downloaded_packages

The downloaded binary packages are in

/var/folders/mg/f7gk10vj1_153rz1zkvd13_00000gn/T//RtmpprnLpL/downloaded_packages

The downloaded binary packages are in

/var/folders/mg/f7gk10vj1_153rz1zkvd13_00000gn/T//RtmpprnLpL/downloaded_packages

The downloaded binary packages are in

/var/folders/mg/f7gk10vj1_153rz1zkvd13_00000gn/T//RtmpprnLpL/downloaded_packages

The downloaded binary packages are in

/var/folders/mg/f7gk10vj1_153rz1zkvd13_00000gn/T//RtmpprnLpL/downloaded_packages

The downloaded binary packages are in

/var/folders/mg/f7gk10vj1_153rz1zkvd13_00000gn/T//RtmpprnLpL/downloaded_packages

The downloaded binary packages are in

/var/folders/mg/f7gk10vj1_153rz1zkvd13_00000gn/T//RtmpprnLpL/downloaded_packages

Advanced Regression Modelling¶

Best Practices and Key Takeaways¶

Always check model assumptions using diagnostic plots (Tukey-Anscombe, Normal Q-Q, Scale-Location, Residual vs Leverage). The enhanced diagnostic plots with simulation envelopes (

plot.glmSim()) provide rigorous checks against model assumptions.Transform variables when appropriate using Tukey’s First-Aid Transformations (log for positive continuous, square-root for counts, logit for proportions). These often lead to simpler, more interpretable models.

Use AIC for model selection, not just p-values from marginal tests. Remember that AIC is for model selection, not hypothesis testing.

Check for overdispersion in count data and use quasi-models if needed. The quasi-Poisson and quasi-binomial families account for extra variation.

Validate models using cross-validation, PRESS, or other validation techniques. The

cv.glm()function provides k-fold cross-validation.Interpret coefficients in the context of the link function (e.g., odds ratios for logistic, multiplicative effects for log link). For logistic regression, always predict on the link scale and transform back to ensure valid confidence intervals.

Make predictions on the appropriate scale (response vs. link). For GLMs with non-linear link functions, the link scale is often more stable for prediction and confidence intervals.

Foundations of Regression Analysis¶

Regression modelling is the art of explaining or modelling the relationship between a response variable and one or more explanatory variables (predictors) , where the relationship is masked by random noise. The goal is to identify a function such that , where represents random variation.

Multiple Linear Regression Model:

Where:

is the response (must be continuous)

are predictors (can be continuous, discrete, binary, or categorical)

are independent error terms

are unknown regression coefficients

Matrix Form:

Model Assumptions:

Linearity: The relationship between predictors and response is linear in parameters

Independence: Errors are stochastically independent

Homoscedasticity: Constant variance across all levels of predictors

Normality: Errors are normally distributed

No Perfect Multicollinearity: Predictors are not linearly dependent

Data Transformation: Tukey’s First-Aid Transformations¶

When the relationship between variables is non-linear or the distribution is skewed, transformations can often linearize the relationship and stabilize variance. Mosteller and Tukey (1977) recommend these first-aid transformations as a starting point:

| Variable Type | Transformation | When to Use | Example |

|---|---|---|---|

| Positive continuous (concentrations, amounts) | Logarithm | Right-skewed data, multiplicative relationships | log(x), log10(x) |

| Count data | Square-root | Poisson-like data with variance ≈ mean | sqrt(x) |

| Counted fractions/proportions | Logit | Percentages (0-100%) | log((x+0.005)/(1.01-x)) |

Why Transform?

Linearize relationships: Makes non-linear patterns linear

Stabilize variance: Addresses heteroscedasticity

Normalize residuals: Helps meet normality assumption

Improve interpretability: Coefficients represent multiplicative effects

Notebook Cell

# Load and explore mtcars data

library(datasets)

str(mtcars)

summary(mtcars)'data.frame': 32 obs. of 11 variables:

$ mpg : num 21 21 22.8 21.4 18.7 18.1 14.3 24.4 22.8 19.2 ...

$ cyl : num 6 6 4 6 8 6 8 4 4 6 ...

$ disp: num 160 160 108 258 360 ...

$ hp : num 110 110 93 110 175 105 245 62 95 123 ...

$ drat: num 3.9 3.9 3.85 3.08 3.15 2.76 3.21 3.69 3.92 3.92 ...

$ wt : num 2.62 2.88 2.32 3.21 3.44 ...

$ qsec: num 16.5 17 18.6 19.4 17 ...

$ vs : num 0 0 1 1 0 1 0 1 1 1 ...

$ am : num 1 1 1 0 0 0 0 0 0 0 ...

$ gear: num 4 4 4 3 3 3 3 4 4 4 ...

$ carb: num 4 4 1 1 2 1 4 2 2 4 ...

mpg cyl disp hp

Min. :10.40 Min. :4.000 Min. : 71.1 Min. : 52.0

1st Qu.:15.43 1st Qu.:4.000 1st Qu.:120.8 1st Qu.: 96.5

Median :19.20 Median :6.000 Median :196.3 Median :123.0

Mean :20.09 Mean :6.188 Mean :230.7 Mean :146.7

3rd Qu.:22.80 3rd Qu.:8.000 3rd Qu.:326.0 3rd Qu.:180.0

Max. :33.90 Max. :8.000 Max. :472.0 Max. :335.0

drat wt qsec vs

Min. :2.760 Min. :1.513 Min. :14.50 Min. :0.0000

1st Qu.:3.080 1st Qu.:2.581 1st Qu.:16.89 1st Qu.:0.0000

Median :3.695 Median :3.325 Median :17.71 Median :0.0000

Mean :3.597 Mean :3.217 Mean :17.85 Mean :0.4375

3rd Qu.:3.920 3rd Qu.:3.610 3rd Qu.:18.90 3rd Qu.:1.0000

Max. :4.930 Max. :5.424 Max. :22.90 Max. :1.0000

am gear carb

Min. :0.0000 Min. :3.000 Min. :1.000

1st Qu.:0.0000 1st Qu.:3.000 1st Qu.:2.000

Median :0.0000 Median :4.000 Median :2.000

Mean :0.4062 Mean :3.688 Mean :2.812

3rd Qu.:1.0000 3rd Qu.:4.000 3rd Qu.:4.000

Max. :1.0000 Max. :5.000 Max. :8.000 # Apply Tukey's First-Aid Transformations

mtcars1 <- data.frame(

lMPG = log(mtcars$mpg), lDisp = log(mtcars$disp), lHP = log(mtcars$hp), lWT = log(mtcars$wt), wCarb = sqrt(mtcars$carb), wCyl = sqrt(mtcars$cyl), wGear = sqrt(mtcars$gear), drat = mtcars$drat, qsec = mtcars$qsec, vs = mtcars$vs, am = mtcars$am)Output

Model Fitting and Inference¶

Least Squares Estimation: The ordinary least squares (OLS) estimator minimizes the sum of squared residuals:

This is equivalent to the maximum likelihood estimator when errors are normally distributed.

# Fit linear model

model <- lm(lMPG ~ lDisp + wGear + am, data = mtcars1)

summary(model)

Call:

lm(formula = lMPG ~ lDisp + wGear + am, data = mtcars1)

Residuals:

Min 1Q Median 3Q Max

-0.22846 -0.09056 -0.00933 0.08235 0.32026

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 5.43775 0.50879 10.688 2.17e-11 ***

lDisp -0.46064 0.05328 -8.647 2.15e-09 ***

wGear -0.02494 0.21158 -0.118 0.907

am 0.00452 0.08608 0.053 0.958

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 0.1326 on 28 degrees of freedom

Multiple R-squared: 0.8208, Adjusted R-squared: 0.8016

F-statistic: 42.76 on 3 and 28 DF, p-value: 1.39e-10

Variable Selection with AIC¶

When many predictors appear non-significant, model selection helps find the simplest adequate model. Akaike’s Information Criterion (AIC) balances model fit and complexity:

Where is the total number of estimated parameters (including ).

Interpretation: Lower AIC = better model (rewards fit, penalizes complexity)

# Stepwise selection (both directions)

full.model <- lm(lMPG ~ lDisp + lHP + lWT + drat + qsec + wCarb + wCyl + wGear + vs + am,

data = mtcars1)

step.model <- step(full.model, direction = "both")

# or: direction="forward" to only add terms

# or: direction="backward" to only remove terms

# Compare AIC values

AIC(full.model) # -38.0116232029208 (more complex)

AIC(step.model) # -48.3532763205495 (simpler, better fit)Output

Start: AIC=-130.82

lMPG ~ lDisp + lHP + lWT + drat + qsec + wCarb + wCyl + wGear +

vs + am

Df Sum of Sq RSS AIC

- drat 1 0.000040 0.26986 -132.82

- qsec 1 0.002350 0.27217 -132.55

- vs 1 0.002637 0.27246 -132.51

- am 1 0.003992 0.27381 -132.35

- wCyl 1 0.009593 0.27941 -131.71

- lDisp 1 0.011167 0.28099 -131.53

<none> 0.26982 -130.82

- lHP 1 0.017922 0.28774 -130.77

- wCarb 1 0.021488 0.29131 -130.37

- lWT 1 0.029303 0.29912 -129.53

- wGear 1 0.037225 0.30704 -128.69

Step: AIC=-132.82

lMPG ~ lDisp + lHP + lWT + qsec + wCarb + wCyl + wGear + vs +

am

Df Sum of Sq RSS AIC

- qsec 1 0.002313 0.27217 -134.55

- vs 1 0.002606 0.27247 -134.51

- am 1 0.003955 0.27381 -134.35

- wCyl 1 0.009768 0.27963 -133.68

- lDisp 1 0.011133 0.28099 -133.53

<none> 0.26986 -132.82

- lHP 1 0.019281 0.28914 -132.61

- wCarb 1 0.022980 0.29284 -132.20

- lWT 1 0.029993 0.29985 -131.45

+ drat 1 0.000040 0.26982 -130.82

- wGear 1 0.037507 0.30736 -130.66

Step: AIC=-134.55

lMPG ~ lDisp + lHP + lWT + wCarb + wCyl + wGear + vs + am

Df Sum of Sq RSS AIC

- vs 1 0.001432 0.27360 -136.38

- am 1 0.007305 0.27948 -135.70

- wCyl 1 0.008183 0.28035 -135.60

- lDisp 1 0.016096 0.28827 -134.71

<none> 0.27217 -134.55

- lHP 1 0.023733 0.29590 -133.87

- wCarb 1 0.031691 0.30386 -133.02

- lWT 1 0.032500 0.30467 -132.94

+ qsec 1 0.002313 0.26986 -132.82

+ drat 1 0.000003 0.27217 -132.55

- wGear 1 0.037537 0.30971 -132.41

Step: AIC=-136.38

lMPG ~ lDisp + lHP + lWT + wCarb + wCyl + wGear + am

Df Sum of Sq RSS AIC

- am 1 0.005878 0.27948 -137.70

- wCyl 1 0.010821 0.28442 -137.14

- lDisp 1 0.014664 0.28827 -136.71

<none> 0.27360 -136.38

- lHP 1 0.025731 0.29934 -135.50

- wCarb 1 0.030412 0.30402 -135.00

+ vs 1 0.001432 0.27217 -134.55

+ qsec 1 0.001139 0.27247 -134.51

- wGear 1 0.036105 0.30971 -134.41

- lWT 1 0.036238 0.30984 -134.40

+ drat 1 0.000000 0.27360 -134.38

Step: AIC=-137.7

lMPG ~ lDisp + lHP + lWT + wCarb + wCyl + wGear

Df Sum of Sq RSS AIC

- wCyl 1 0.0083098 0.28779 -138.76

- lDisp 1 0.0118540 0.29134 -138.37

<none> 0.27948 -137.70

- wCarb 1 0.0292247 0.30871 -136.51

- lHP 1 0.0293416 0.30882 -136.50

- wGear 1 0.0304382 0.30992 -136.39

+ am 1 0.0058778 0.27360 -136.38

- lWT 1 0.0311628 0.31064 -136.31

+ qsec 1 0.0043786 0.27510 -136.20

+ drat 1 0.0001631 0.27932 -135.72

+ vs 1 0.0000050 0.27948 -135.70

Step: AIC=-138.76

lMPG ~ lDisp + lHP + lWT + wCarb + wGear

Df Sum of Sq RSS AIC

- lDisp 1 0.004577 0.29237 -140.25

<none> 0.28779 -138.76

- wCarb 1 0.020996 0.30879 -138.51

- wGear 1 0.022152 0.30994 -138.39

- lHP 1 0.024521 0.31231 -138.14

+ wCyl 1 0.008310 0.27948 -137.70

+ am 1 0.003367 0.28442 -137.14

+ vs 1 0.000951 0.28684 -136.87

+ qsec 1 0.000941 0.28685 -136.87

+ drat 1 0.000842 0.28695 -136.85

- lWT 1 0.055166 0.34296 -135.15

Step: AIC=-140.26

lMPG ~ lHP + lWT + wCarb + wGear

Df Sum of Sq RSS AIC

- wCarb 1 0.017460 0.30983 -140.40

<none> 0.29237 -140.25

- wGear 1 0.029021 0.32139 -139.23

+ lDisp 1 0.004577 0.28779 -138.76

+ qsec 1 0.003739 0.28863 -138.67

+ am 1 0.002699 0.28967 -138.55

+ wCyl 1 0.001033 0.29134 -138.37

+ drat 1 0.000498 0.29187 -138.31

+ vs 1 0.000003 0.29237 -138.26

- lHP 1 0.103033 0.39540 -132.59

- lWT 1 0.127849 0.42022 -130.65

Step: AIC=-140.4

lMPG ~ lHP + lWT + wGear

Df Sum of Sq RSS AIC

- wGear 1 0.012179 0.32201 -141.16

<none> 0.30983 -140.40

+ wCarb 1 0.017460 0.29237 -140.25

+ qsec 1 0.010958 0.29887 -139.55

+ drat 1 0.003949 0.30588 -138.81

+ am 1 0.003826 0.30600 -138.80

+ vs 1 0.001547 0.30828 -138.56

+ lDisp 1 0.001041 0.30879 -138.51

+ wCyl 1 0.000060 0.30977 -138.41

- lWT 1 0.209549 0.51938 -125.87

- lHP 1 0.221250 0.53108 -125.16

Step: AIC=-141.17

lMPG ~ lHP + lWT

Df Sum of Sq RSS AIC

<none> 0.32201 -141.16

+ wGear 1 0.01218 0.30983 -140.40

+ qsec 1 0.00715 0.31486 -139.88

+ lDisp 1 0.00664 0.31537 -139.83

+ wCyl 1 0.00351 0.31849 -139.52

+ vs 1 0.00222 0.31979 -139.39

+ wCarb 1 0.00062 0.32139 -139.23

+ am 1 0.00036 0.32165 -139.20

+ drat 1 0.00013 0.32187 -139.18

- lHP 1 0.21221 0.53422 -126.97

- lWT 1 0.45939 0.78140 -114.80

# Cross-validation

library(boot)

step.model.glm <- glm(step.model$terms,

data = model.frame(step.model),

family = gaussian)

cv.error <- cv.glm(mtcars1, step.model.glm, K = 11)

cv.error$delta[1] # Mean cross-validated errorOutput

Handling Categorical Predictors¶

Categorical variables (factors) require special handling in regression models.

Dummy Coding (Treatment Contrasts):

Creates k-1 binary variables for a factor with k levels

Each coefficient represents the difference from the reference level

Other Contrast Types:

Sum-to-zero:

contr.sum()- coefficients sum to zeroHelmert:

contr.helmert()- compares each level to mean of subsequent levelsPolynomial:

contr.poly()- for ordered factors

# Automatic dummy coding

lm(mpg ~ factor(cyl) + hp, data = mtcars)

# Change reference level

mtcars$cyl_f <- relevel(factor(mtcars$cyl), ref = "6")

lm(mpg ~ cyl_f + hp, data = mtcars)Output

Call:

lm(formula = mpg ~ factor(cyl) + hp, data = mtcars)

Coefficients:

(Intercept) factor(cyl)6 factor(cyl)8 hp

28.65012 -5.96766 -8.52085 -0.02404

Call:

lm(formula = mpg ~ cyl_f + hp, data = mtcars)

Coefficients:

(Intercept) cyl_f4 cyl_f8 hp

22.68246 5.96766 -2.55320 -0.02404

Detecting Multicollinearity¶

Multicollinearity occurs when predictors are highly correlated, making it difficult to estimate individual coefficients reliably.

Variance Inflation Factor (VIF):

Where is the coefficient of determination from regressing predictor j on all other predictors.

Interpretation:

VIF ≈ 1: No collinearity

VIF > 5: Moderate collinearity (concerning)

VIF > 10: Severe collinearity (problematic)

Solutions for Multicollinearity:

Remove one of the correlated predictors (if theoretically justified)

Combine predictors (e.g., create an index)

Use ridge regression or other regularization methods

Accept it if the goal is prediction, not inference

library(car)

vif(model) # VIF for each predictorOutput

Model Validation Techniques¶

Cross-Validation:

Split data into training and test sets

Fit model on training, evaluate on test

k-fold CV: Split into k folds, use each as test set once

PRESS (Predicted Residual Sum of Squares):

Where is the predicted value when observation i is left out.

model <- glm(lMPG ~ lDisp + lHP + lWT + drat + qsec + wCarb + wCyl + wGear + vs + am,

data = mtcars1,

family = gaussian)

# k-fold cross-validation

library(boot)

cv.error <- cv.glm(mtcars1, model, K = 10)

cv.error$delta[1] # MSE: 0.0154950441014118

# PRESS statistic

press <- sum(residuals(model) / (1 - hatvalues(model)))^2

press # 0.0168671439271504Output

Advanced Topics in Linear Regression¶

Weighted Least Squares (WLS)¶

When variance is not constant (heteroscedasticity), WLS assigns different weights to observations:

Where if the variance structure is known.

# Weights inversely proportional to variance

weights <- 1 / fitted(model)^2

wls.model <- lm(mpg ~ wt + hp, data = mtcars, weights = weights)Robust Fitting¶

Robust regression reduces the influence of outliers and leverage points using robust loss functions:

Huber: Less sensitive to outliers than squared loss

Tukey bisquare: Even more robust, completely ignores extreme outliers

Huber with M-estimation: Iteratively reweighted least squares

library(MASS)

# Robust linear model

robust.model <- rlm(mpg ~ wt + hp, data = mtcars)

# Compare with OLS

summary(robust.model)

coef(robust.model) # More resistant to outliersOutput

Call: rlm(formula = mpg ~ wt + hp, data = mtcars)

Residuals:

Min 1Q Median 3Q Max

-3.6639 -1.3057 0.1727 1.3162 6.3392

Coefficients:

Value Std. Error t value

(Intercept) 36.5840 1.4380 25.4407

wt -3.8801 0.5691 -6.8180

hp -0.0293 0.0081 -3.6050

Residual standard error: 2.006 on 29 degrees of freedomFitting Smooth Functions¶

Non-parametric smoothing captures non-linear relationships without specifying a functional form:

LOESS (Locally Estimated Scatterplot Smoothing):

Fits local polynomials using weighted regression

Span parameter: Controls smoothness (larger = smoother)

Splines:

Natural cubic splines: Smooth, flexible functions

B-splines: Local support, computationally efficient

# LOESS smoothing

loess.model <- loess(mpg ~ hp, data = mtcars, span = 0.75)

# Natural cubic splines with 3 degrees of freedom

library(splines)

ns.hp <- ns(mtcars$hp, df = 3)Additive Models¶

Additive models extend linear regression by allowing non-linear relationships:

Where are smooth functions (can be linear, splines, LOESS, etc.).

Advantages:

Flexible non-linear relationships

Additive structure (easy to interpret each term)

Automatic smoothness selection

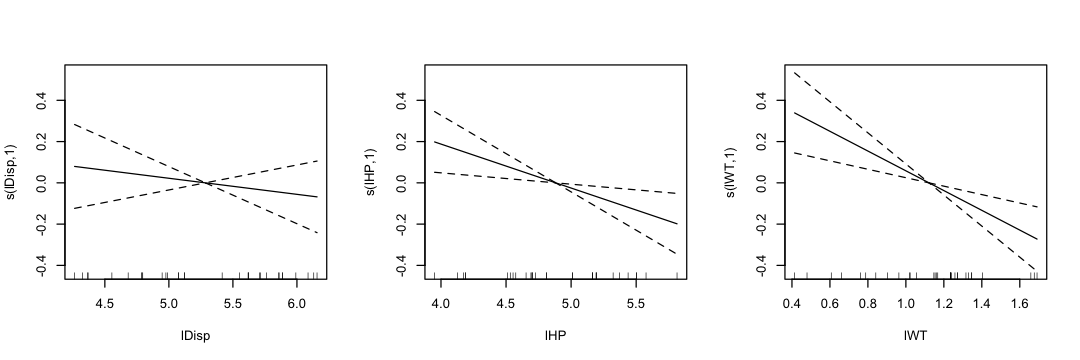

library(mgcv)

# Fit additive model

gam.model <- gam(lMPG ~ s(lDisp) + s(lHP) + s(lWT),

data = mtcars1)

# Summary with estimated degrees of freedom

# summary(gam.model)

# Plot smooth terms

par(mfrow = c(1, 3))

plot(gam.model, se = TRUE)

Binary Response: Logistic Regression¶

When the response is binary (success/failure, yes/no), ordinary linear regression is inappropriate because:

Predictions can fall outside [0, 1]

The linear model assumes constant variance, but binary data has variance that depends on the mean

The distribution is binomial, not normal

Logistic Regression Model

Where is the linear predictor.

Logit Link Function

Interpretation of Coefficients

= change in log-odds per unit change in

= odds ratio (multiplicative change in odds)

If : Higher increases probability of success

If : Higher decreases probability of success

Generalized Linear Models (GLM)¶

GLMs unify various regression models under a single framework (Nelder & Wedderburn, 1972). They consist of three components:

Random Component: Response follows a distribution from the exponential family

Systematic Component: Linear predictor

Link Function: , where

Exponential Family¶

The dispersion parameter is connected to the variance

The value is a fixed known number (weighting)

The function scales the probability to 1.

The functions and determine the distribution.

Expected Value:

where and are the first derivatives with respect to .

Variance:

| Distribution | Range of | Link | |||||

|---|---|---|---|---|---|---|---|

| Gaussian | 1 | 1 | |||||

| prop; Binomial | 1 | ||||||

| counts; Binomial | 1 | 1 | |||||

| Poisson | 1 | 1 | |||||

| Gamma | 1 | ||||||

| Inverse Gauss. | 1 |

Distribution: The probability distribution of the response variable ;Defines the random component of the GLM

Range of : The support (set of possible values) for the response variable; Determines which distribution is appropriate for your data

: The expected value (mean) of the response; The target of your regression model

: The variance of the response variable; Determines precision of estimates

: The canonical link function from the exponential family density;

: The variance function; Connects mean to variance:

: The dispersion parameter; Scales the variance: larger means more spread

: The prior weight for each observation; Known constant for each observation (e.g., for binomial)

# Fit logistic regression model

chal.glm <- glm(cbind(Fails, m-Fails) ~ Temp + Pres,

family = binomial(link = logit),

data = chal)

summary(chal.glm)

# Odds ratios

exp(coef(chal.glm))Output

Call:

glm(formula = cbind(Fails, m - Fails) ~ Temp + Pres, family = binomial(link = logit),

data = chal)

Coefficients:

Estimate Std. Error z value Pr(>|z|)

(Intercept) 3.409728 3.178539 1.073 0.2834

Temp -0.107747 0.044648 -2.413 0.0158 *

Pres 0.007380 0.006447 1.145 0.2523

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

(Dispersion parameter for binomial family taken to be 1)

Null deviance: 24.230 on 22 degrees of freedom

Residual deviance: 16.565 on 20 degrees of freedom

AIC: 36.125

Number of Fisher Scoring iterations: 5

Temperature coefficient: -0.1077 (p = 0.0158)

Interpretation: Each 1F decrease in temperature multiplies the odds of failure by (11.4% increase)

Engineering implication: At the launch temperature of 31F (well below previous launches), the failure probability was unacceptably high

Pressure coefficient: 0.0074 (p = 0.2523)

Not statistically significant at 5% level

Hypothesis Test:

Does pressure affect failure probability?

(no effect), (effect exists)

Deviance test (more reliable than Wald for small samples):

# Compare models with and without Pres

chal.glm1 <- glm(cbind(Fails, m-Fails) ~ Pres + Temp,

family = binomial, data = chal)

chal.glm2 <- glm(cbind(Fails, m-Fails) ~ Temp,

family = binomial, data = chal)

anova(chal.glm1, chal.glm2, test = "Chisq")

# Result: p-value = 0.2174 > 0.05Output

Conclusion: Cannot reject → No evidence that pressure affects failure probability

Confidence Interval for Temperature:

confint(chal.glm1)

# Temp: [-0.201, -0.022]Output

95% CI for temperature coefficient: [-0.201, -0.022]

Does not include 0 → confirms significant effect

Principle:

confint()uses deviance test statistic (more reliable than Wald)

Prediction at 31F: The critical question: What was the predicted failure probability at the launch temperature of 31F?

# Predicted probability at 31°F (using average pressure)

new.data <- data.frame(Temp = 31, Pres = mean(chal$Pres))

pred.response <- predict(chal.glm2, newdata = new.data,

type = "response", se = TRUE)

# pred.response$fit: 0.8178 (81.78% probability of failure)Output

# WRONG METHOD (can exceed [0,1]): 95% confidence interval

pred.response$fit + c(-1, 1) * qnorm(0.975) * pred.response$se.fit

# [0.3465, 1.2891] - Invalid! Exceeds [0,1]Output

# CORRECT METHOD: 95% confidence interval

# Predict on link scale, then transform

pred.link <- predict(chal.glm2, newdata = new.data,

type = "link", se = TRUE)

ci.link <- pred.link$fit + c(-1, 1) * qnorm(0.975) * pred.link$se.fit

ci.response <- 1 / (1 + exp(-ci.link)) # [0.1596, 0.9907]Data Selection Lesson: Engineers considered using only data where O-rings showed thermal distress.

Problem: This drops observations with no distress, which contain valuable information

Principle: Never drop data based on the response variable - you never know if it influences the outcome

Solution: Use all available data for analysis

Inference for GLMs¶

Deviances¶

Deviance measures the goodness of fit of a model:

Null deviance: Measures total variation in the response (model with only intercept)

Residual deviance: Measures variation not explained by the model

Difference in deviances: Measures improvement from adding predictors

For nested models, the difference in residual deviances follows a distribution:

Where df = difference in number of parameters.

# Compare nested models

model.full <- glm(Calls ~ Center + Time, family = poisson, data = dial)

model.reduced <- glm(Calls ~ Center, family = poisson, data = dial)

# Deviance test

anova(model.full, model.reduced, test = "Chisq")Output

Overdispersion¶

Overdispersion occurs when the observed variance exceeds what the model assumes:

Poisson: Variance > mean

Binomial: Variance >

Detection:

If , there is evidence of overdispersion.

Example - Poisson GLM with Overdispersion

The warpbreaks dataset contains the number of breaks in yarn during weaving, classified by wool type (A, B) and tension (L, M, H). This is a classic example where overdispersion is present.

Model:

R Output:

Coefficients:

Estimate Std. Error z value Pr(>|z|)

(Intercept) 3.7967 0.0499 76.030 <2e-16 ***

woolB -0.4566 0.0802 -5.694 1.24e-08 ***

tensionM -0.6187 0.0844 -7.330 2.30e-13 ***

tensionH -0.5958 0.0838 -7.112 1.15e-12 ***

woolB:tensionM 0.6382 0.1222 5.224 1.75e-07 ***

woolB:tensionH 0.1884 0.1299 1.450 0.147Interaction Term Significance:

Null: (no interaction)

Alternative: At least one interaction coefficient ≠ 0

Test: Deviance test (drop1 with Chisq test)

R Code:

# Test interaction term

drop1(WB.glm, test="Chisq")

# Result: p-value = 7.962e-07 < 0.05Conclusion: Interaction term is needed to explain the response

Overdispersion Detection:

Definition: More dispersion in the data than the Poisson model allows (Poisson assumes mean = variance)

Detection: Residual deviance / residual df = 182.31 / 48 = 3.798

Test:

1 - pchisq(182.31, 48) = 0(essentially 0) < 0.05Conclusion: Strong evidence of overdispersion

Implications:

The Poisson model is not adequate to describe the data

Statistical conclusions based on this model (including the interaction test) are not valid

Solution: Use a quasi-Poisson model to account for overdispersion

Modified Model:

# Quasi-Poisson regression

WB.qPReg1 <- glm(breaks ~ wool*tension,

family = quasipoisson,

data = warpbreaks)

WB.qPReg1Output

Call: glm(formula = breaks ~ wool * tension, family = quasipoisson,

data = warpbreaks)

Coefficients:

(Intercept) woolB tensionM tensionH woolB:tensionM

3.7967 -0.4566 -0.6187 -0.5958 0.6382

woolB:tensionH

0.1884

Degrees of Freedom: 53 Total (i.e. Null); 48 Residual

Null Deviance: 297.4

Residual Deviance: 182.3 AIC: NAConfidence Intervals for GLMs¶

Wald-type Confidence Intervals¶

!! Assumes normal sampling distribution !!

| Confidence Level | z-score (qnorm(p)) | |

|---|---|---|

| 90% | 0.10 | |

| 95% | 0.05 | |

| 99% | 0.01 |

Based on asymptotic normality of MLEs

Simple to compute but can be inaccurate for small samples or sparse data

May produce invalid ranges (e.g., probabilities outside [0,1])

Deviance-based Confidence Intervals¶

!! For GLMs, always prefer this likelihood-based approach over Wald by hand - it’s more accurate !!

Based on likelihood ratio tests

More reliable for small samples

Guarantees intervals stay within valid range

# For GLMs, R uses Deviance-based methods by default with non-Gaussian families.

# For LMs, R uses confint.lm() that employs the t-distribution instead of the normal.

# For others, Wald is the default method

# Deviance-based (more reliable than Wald)

confint(model, method = "profile")Output

Diagnostics and Model Adequacy Checking¶

Model adequacy is crucial - a model is only as good as its assumptions. Diagnostic plots help verify these assumptions.

Essential Diagnostic Plots for GLMs¶

Tukey-Anscombe Plot (Residuals vs Fitted):

Check: Linear relationship, constant variance

Problem: Non-linear pattern → missing non-linear term

Problem: Funnel shape → heteroscedasticity

Normal Q-Q Plot (Quantiles of residuals vs theoretical):

Check: Normality of residuals

Problem: Points deviate from line → non-normal residuals

Problem: Heavy tails → outliers

Scale-Location Plot ( vs Fitted):

Check: Constant variance

Problem: Non-constant spread → heteroscedasticity

Residual vs Leverage:

Check: Influential observations

Problem: Cook’s distance > 1 → too influential

Problem: High leverage points → extrapolation

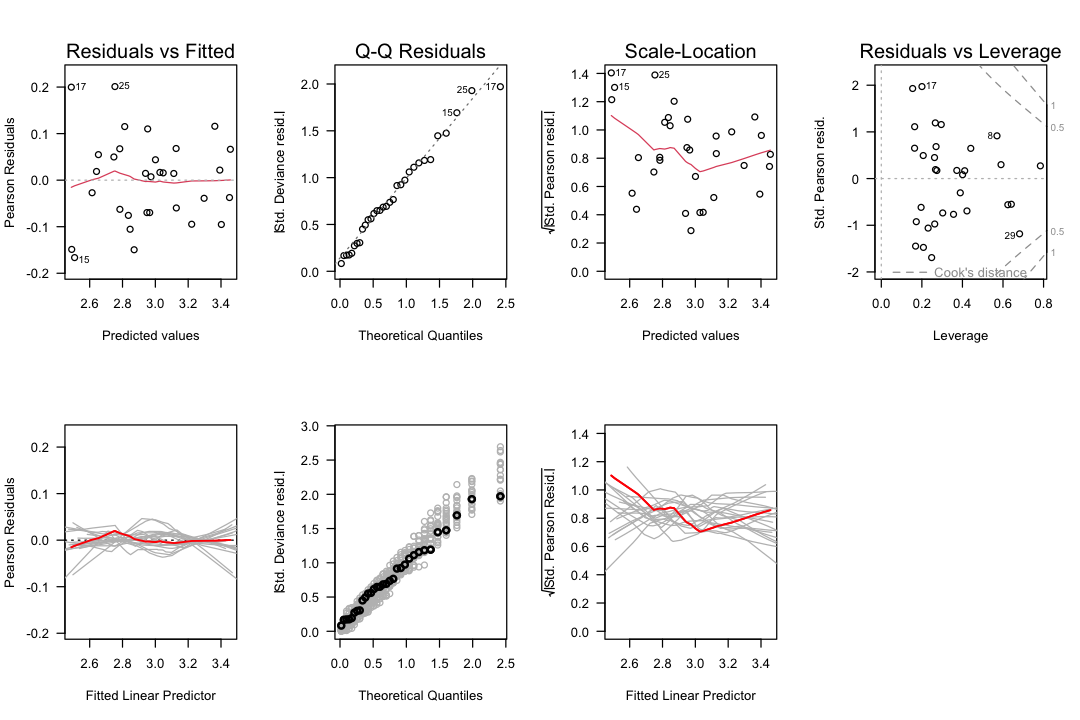

Enhanced Diagnostics with Simulation¶

Simulated envelopes provide a more rigorous check by comparing observed diagnostic curves to what we’d expect under the model assumptions:

# Enhanced diagnostic plots with simulation (RFn_Plot-glmSim.R loaded in setup)

par(mfrow = c(2, 4), las = 1)

plot(model)

plot.glmSim(model, SEED = 4711)

Interpretation:

If observed curves fall within the gray envelope (simulated fluctuation), there is no evidence against the assumption

If observed curves fall outside the envelope, there is evidence the assumption is violated

Example - Machine Failures Residual Analysis:

A machinery runs in two modes. The question is whether the number of failures depends on operating time in each mode. After fitting a Poisson regression model, we perform a residual and sensitivity analysis.

Diagnostic Plots Interpretation:

Tukey-Anscombe Plot: Smoother indicates some non-constant expectation, but within stochastic fluctuation (gray spaghetti) → Weak evidence against adequately specified expectation

Location-Scale Plot: Smoother decreasing but within stochastic fluctuation → No evidence against adequately specified variance

Normal Q-Q Plot: Points scatter around line, all black points within gray points → No evidence for outliers or distributional violations

Residual vs Leverage: All Cook’s distances < 1 → No observation with too large influence

Overall Conclusion: Model might be adequate, though there’s a weak hint that expectation might not be constant (but limited data prevents strong conclusions).

Statistical Soundness: Because there is no serious evidence against model assumptions, the statistical conclusions from the hypothesis test and overdispersion check are valid.

Example - Residual Analysis with Simulation:

The six diagnostic plots (Tukey-Anscombe, Normal Q-Q, Scale-Location) with simulation envelopes (gray lines and points) provide additional insights.

Purpose of Gray Lines and Points:

Gray lines: Show the scatter range of the smoother under model assumptions

Gray points: Show the scatter range of data points under model assumptions

Interpretation: If black (observed) structures lie outside the gray (simulated) structures, this is evidence the model does not adequately describe the data

Residual and Sensitivity Analysis for Yarn Breaks:

Tukey-Anscombe Plot:

Observation: Smoother is a reasonably straight horizontal line

Comparison: Within stochastic fluctuation (gray spaghetti)

Conclusion: No evidence that expectation is incorrectly specified

Normal Q-Q Plot:

Observation: Black points are not within stochastic fluctuation (gray points)

Interpretation: Evidence of distortions of the distributional assumption

Art of violation: Suggests overdispersion

Scale-Location Plot:

Observation: Red smoother has a weak trend, shifted upwards

Comparison: Outside stochastic fluctuation

Conclusion: Evidence that variance is incorrectly specified

Art of violation: Suggests overdispersion

Overall Conclusion: There is evidence that the model does not fit the data adequately. The identified violations suggest overdispersion is the main issue, which we addressed by using a quasi-Poisson model.

Residual Types for GLMs:

Response residuals: (observed - predicted)

Pearson residuals: (standardized)

Deviance residuals: Contribute to deviance statistic

# Extract different residual types

residuals(model, type = "response")

residuals(model, type = "pearson")

residuals(model, type = "deviance")Output

Model Improvement: Finding Appropriate Transformations¶

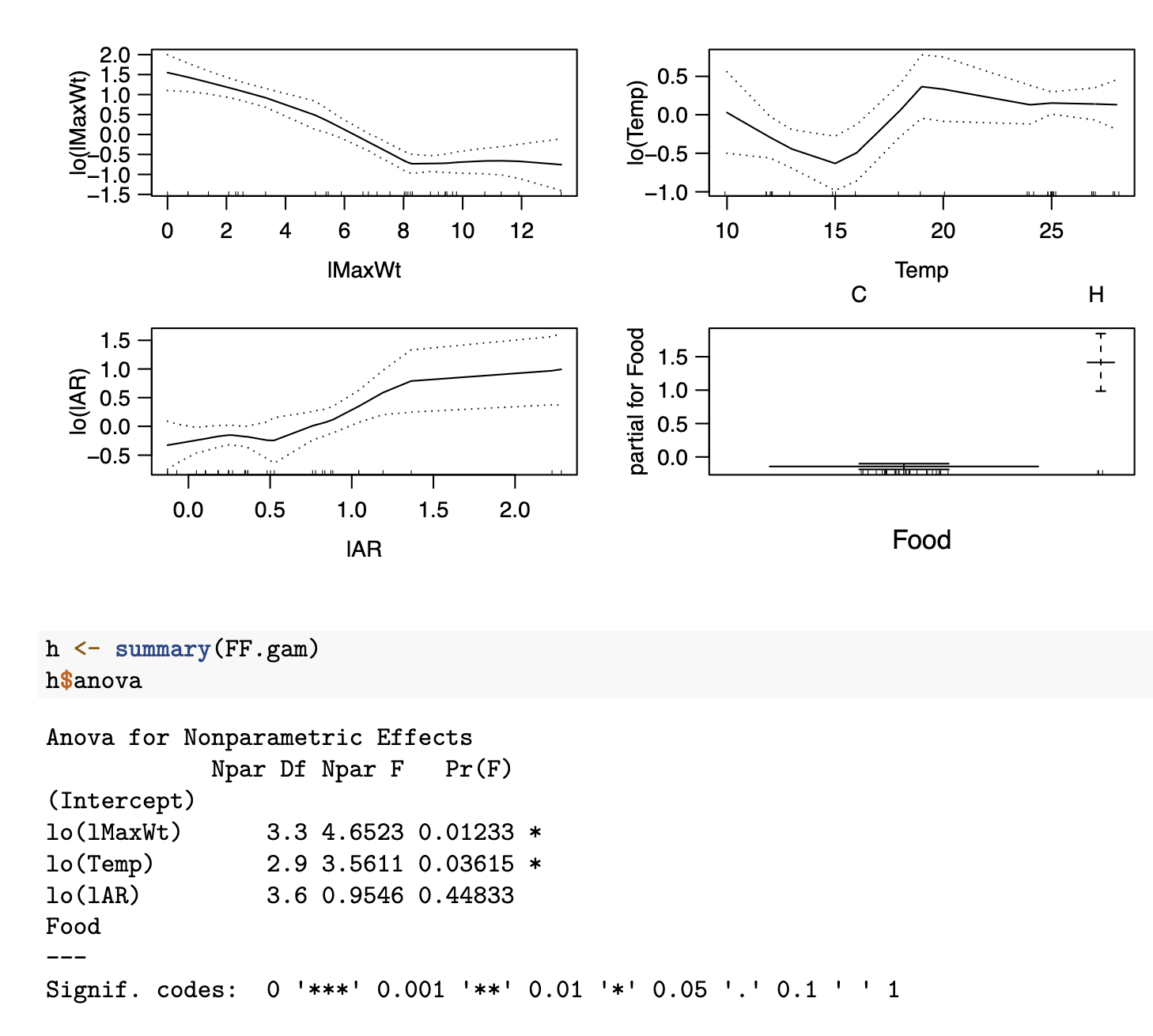

Generalized Additive Models (GAMs) are excellent for exploring non-linear relationships in a data-driven manner:

Rule of Thumb: Predictor needs a transformation if a straight line does not fit between the confidence band or the P-value of the coresponding coefficient in Anova for Nonparametric Effects is smaller than 0.05

lMaxWtneeds an additional transformation; Hockeystick with L at 8Tempneeds a transformation as well: possible a factor variable withiTemp=0ifTemp < 17,iTemp=1otherwiselAR: no additional transformation is neededFoodis a factor variable and cannot be transformed in any case

Extensions of GLMs¶

Rate Models¶

Rate models analyze counts per unit exposure (e.g., accidents per kilometer driven, failures per machine-hour):

Where is the exposure (offset).

# Poisson regression with offset for ship damage data

glm(Damages ~ Year + Month + offset(log(Exposure)),

family = poisson,

data = ship)

Call: glm(formula = Damages ~ Year + Month + offset(log(Exposure)),

family = poisson, data = ship)

Coefficients:

(Intercept) Year65 Year70 Year75 Month75

-5.5607 -0.3086 0.2649 -18.2099 NA

Degrees of Freedom: 19 Total (i.e. Null); 16 Residual

Null Deviance: 13.64

Residual Deviance: 10.54 AIC: 26.54Interpretation: The offset ensures we’re modeling the rate (counts per unit exposure) rather than raw counts.

Quasi-Likelihood Models¶

Quasi-models extend GLMs when the full distribution is not specified, requiring only the mean-variance relationship:

Quasi-Poisson:

Where is the dispersion parameter estimated from data.

# Quasi-Poisson for overdispersed count data

qp.model <- glm(breaks ~ wool * tension,

family = quasipoisson,

data = warpbreaks)

summary(qp.model)

# Dispersion parameter

qp.model$dispersion # Should be > 1 if overdispersedOutput

Call:

glm(formula = breaks ~ wool * tension, family = quasipoisson,

data = warpbreaks)

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 3.79674 0.09688 39.189 < 2e-16 ***

woolB -0.45663 0.15558 -2.935 0.005105 **

tensionM -0.61868 0.16374 -3.778 0.000436 ***

tensionH -0.59580 0.16253 -3.666 0.000616 ***

woolB:tensionM 0.63818 0.23699 2.693 0.009727 **

woolB:tensionH 0.18836 0.25201 0.747 0.458436

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

(Dispersion parameter for quasipoisson family taken to be 3.76389)

Null deviance: 297.37 on 53 degrees of freedom

Residual deviance: 182.31 on 48 degrees of freedom

AIC: NA

Number of Fisher Scoring iterations: 4

NULLCausality¶

Best Practices and Key Takeaways¶

Distinguish association from causation - correlation does not imply causation. The shoe size and salary example demonstrates how a common cause (gender) can create spurious associations.

Use DAGs to represent causal assumptions explicitly. Nodes are variables, directed edges are potential causal effects. Use the

gRbaseandgRainpackages to work with DAGs and Bayesian networks.Identify confounders and adjust for them appropriately using the backdoor criterion. The Nutrition-Disease example shows how to find valid adjustment sets.

Use d-separation to determine conditional independencies in the graph. The sprinkler network example illustrates the three basic structures (chain, fork, collider) and their independence properties.

Apply the backdoor criterion to find valid adjustment sets for causal effect estimation. This allows estimating causal effects from observational data when appropriate variables are measured.

Consider counterfactuals for individual-level causal questions using Pearl’s three-step method (abduction, action, prediction). The online sales example demonstrates practical counterfactual reasoning.

Validate causal models through sensitivity analysis, robustness checks, and external validation. Always question whether the causal assumptions are reasonable and test the stability of results.

Why Causal Inference Matters¶

Traditional statistics and machine learning excel at finding associations and making predictions, but they cannot answer causal questions without additional assumptions. Causal inference is essential when we want to understand what would happen if we changed something.

Key Distinction:

Association: - What is the probability of Y given X? Do people who drink more coffee tend to be more productive?

Intervention: - What would Y be if we set X to x? If I drink 20 cups of coffee, will I be more productive?

Counterfactual: - What would Y have been if X had been x, given that X was actually x’ and Y was y’? Would I have been more productive yesterday if I had drunk 20 cups of coffee instead of 2?

The first question can be answered with observational data, but the second and third require causal assumptions.

Causal Graphical Models¶

Causal graphical models (DAGs - Directed Acyclic Graphs) provide a language for representing causal assumptions explicitly.

Components:

Nodes: Random variables

Directed edges: Potential causal effects

Absence of edge: No direct causal effect

Terminology:

Parent: Node with directed edge to another node

Child: Node with directed edge from another node

Ancestor: Node with directed path to another node

Descendant: Node with directed path from another node

Adjacent: Nodes connected by an edge

Example - Bayesian Networks:

Building and querying Bayesian networks using the gRain package:

library(gRain)

# Define CPTs with explicit levels

cptSeason <- cptable(~Season,

values = c(0.5, 0.5),

levels = c("winter", "summer"))

cptSprinkler <- cptable(~Sprinkler | Season, # Use | not :

values = matrix(c(0.5, 0.5, 0.9, 0.1), nrow = 2, byrow = TRUE),

levels = list(Sprinkler = c("off", "on"),

Season = c("winter", "summer")))

# Build network

bn <- compileCPT(list(Season = cptSeason, Sprinkler = cptSprinkler))

bn <- grain(bn)

# Query probabilities

# querygrain(bn, nodes = c("Season"), type = "marginal")

# querygrain(bn, nodes = c("Season", "Sprinkler"), type = "conditional")Graphical Building Blocks:

Chain (Mediation):

X affects Y through Z

Example: Education → Income → Happiness

Fork (Confounding):

Z is a common cause of X and Y

Example: Gender → (Shoe Size, Salary)

Collider (Selection):

Z is a common effect of X and Y

Example: Rain → Wet ← Sprinkler

Conditional Independence and D-Separation¶

Conditional Independence¶

Two variables X and Y are conditionally independent given Z if:

D-Separation: A path is d-separated (blocked) by a set of nodes Z if it contains a node that is:

Not in Z, and

Is a collider on that path

Two nodes X and Y are d-separated given Z if all paths between them are blocked by Z.

D-Separation Rules¶

| Structure | Independence | Conditional Independence Given Z |

|---|---|---|

| Chain: | Dependent | Independent (blocks chain) |

| Fork: | Dependent | Independent (blocks fork) |

| Collider: | Dependent | Dependent (opens collider) |

DAG Analysis¶

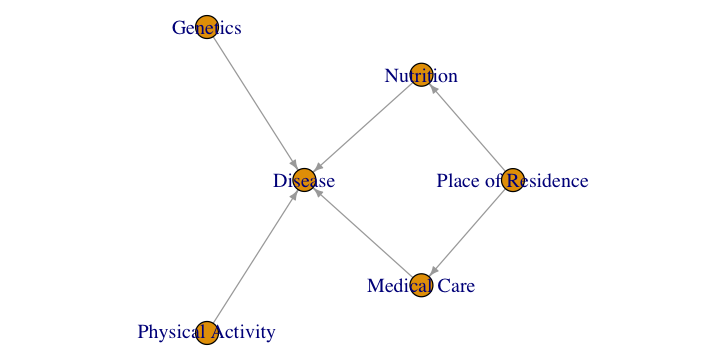

Source

options(repr.plot.width = 6, repr.plot.height = 3)

library(gRbase)

set.seed(253)

g <- dag(

c("Nutrition", "Place of Residence"),

c("Disease", "Medical Care", "Genetics", "Physical Activity", "Nutrition"),

c("Medical Care", "Place of Residence")

)

par(mar = c(0.1, 0.1, 0.1, 0.1))

plot(g)

Descendants of Place of Residence¶

Answer: Medical Care, Nutrition, Disease

Explanation: Descendants are all nodes reachable via directed paths from Place of Residence. From Place of Residence, we can reach Nutrition directly, Medical Care directly, and Disease through Medical Care.

Direct Causal Effect of Place of Residence on Disease¶

Answer: 0

Justification: There is no direct edge from Place of Residence to Disease in the DAG. The effect is only indirect through Medical Care.

Independence Statements¶

i. Nutrition Medical Care | Place of Residence ?

Correct: There is a fork at Place of Residence (common cause of both Nutrition and Medical Care)

Reason: Conditioning on the common cause (Place of Residence) blocks the path between Nutrition and Medical Care, making them conditionally independent

ii. Nutrition Physical Activity | Disease ?

Incorrect: There is a collider at Disease (common effect of Nutrition and Physical Activity)

Reason: Conditioning on the collider (Disease) opens the path between Nutrition and Physical Activity, making them conditionally dependent

iii. Nutrition Genetics | Medical Care ?

Correct: The collider is Disease (not in conditioning set)

Reason: Medical Care is not a descendant of Disease. The collider path (Nutrition Disease Genetics) remains blocked because Disease is not in the conditioning set and Medical Care is not its descendant.

Regression for Total Causal Effect of Nutrition on Disease¶

To estimate the total causal effect of Nutrition on Disease, we must block the backdoor path: Nutrition Place of Residence Medical Care Disease

lm(Disease ~ Nutrition + PlaceOfResidence, data = data)Asymptotically Optimal Adjustment¶

The asymptotically optimal adjustment set minimizes the variance of the causal effect estimator:

= all causal nodes in the directed path from X to Y

= parents of set S

= forbidden nodes (all descendants of causal nodes including X)

Calculation:

(Disease is the only causal neighbor)

(parents of Disease)

(the variables themselves)

Optimal adjustment:

D-Separation Testing¶

Testing conditional independence in DAGs and verifying with data:

Source

options(repr.plot.width = 6, repr.plot.height = 2)

library(gRbase)

d.separates <- function(a,b,c,dag){

separates(a,b,c, moralize(ancestralGraph(union(union(a,b),c),dag)))

}

dag.model <- dag("A",c("B","A","E"),c("C","A","B","D"),c("D","B"),c("E"))

par(mar = c(0.1, 0.1, 0.1, 0.1))

plot(dag.model)

Source

cat("Are E and D d-separated by Z = {B}?", d.separates("E", "D", c("B"), dag.model), "\n")

cat("Are E and C d-separated by Z = {A}?", d.separates("E", "C", c("A"), dag.model), "\n")

cat("Are A and D d-separated by Z = {B, C}?", d.separates("A", "D", c("B", "C"), dag.model), "\n")Are E and D d-separated by Z = {B}? TRUE

Are E and C d-separated by Z = {A}? FALSE

Are A and D d-separated by Z = {B, C}? FALSE

Simpson’s Paradox¶

Simpson’s Paradox occurs when a trend appears in different groups of data but disappears or reverses when these groups are combined.

Example: Layoffs

Overall: More layoffs in Department A than Department B

Within each gender: More layoffs in Department B than Department A

Resolution: Gender distribution differs between departments (more men in A, more women in B, and men are laid off more regardless of department)

Causal Explanation: The paradox arises because gender is a confounder - it affects both the department (exposure) and layoffs (outcome). When we aggregate across genders, the confounding effect creates the paradox.

Solution: Adjust for the confounder (gender) to see the true relationship within each gender group.

Factorization of Joint Distributions¶

For a DAG, the joint distribution factorizes according to the graph structure:

Where are the parents of node in the DAG.

Example: Medical Diagnosis

Where:

D = Disease

S = Symptom

C = Test Result

Interpretation: Disease affects both Symptom and Test Result, but Symptom and Test Result are independent given Disease (d-separated by Disease).

Causal Effect Estimation¶

Causal effect measures how an intervention on X affects Y:

Adjustment Formula: If we can find a set Z that satisfies the backdoor criterion, we can estimate causal effects from observational data:

Backdoor Criterion: A set of variables Z satisfies the backdoor criterion relative to X and Y if:

Z blocks all backdoor paths from X to Y

Z does not contain any descendants of X

Finding Adjustment Sets:

Identify all backdoor paths from X to Y

For each path, find a set that blocks it

Combine these sets, ensuring no new paths are opened

Example - Adjustment Formula:

Estimating causal effects with adjustment: Use backdoor criterion and adjust for all parents of Nutrition that are not descendants.

lm(Disease ~ Nutrition + PlaceOfResidence, data = data)Structural Causal Models (SCMs)¶

Structural Causal Models combine causal graphs with structural equations that describe the data-generating process:

Where:

= endogenous variable

= parents of in the causal graph

= exogenous (noise) variable

= structural function

Linear SCMs:

Direct vs. Total Causal Effects:

Direct effect: Effect of X on Y not mediated through other variables

Total effect: Sum of direct effect + all indirect effects

Example: Linear SCM

Direct effect of X on Y:

Direct effect of X on Z:

Direct effect of Y on Z:

Total effect of X on Z:

Estimating Causal Effects: For linear SCMs, causal effects can be estimated using regression with appropriate adjustment:

# Estimate total causal effect of Nutrition on Disease

# Adjust for confounding variables (Place of Residence)

lm(Disease ~ Nutrition + PlaceOfResidence, data = data)Assumptions of Linear SCMs:

Known causal structure

Linear relationships

Uncorrelated errors

No unmeasured confounders

Limitations:

Requires prior knowledge of causal structure

Linear assumption may not hold

Errors may be correlated in practice

Example - Linear SCMs: Defining and working with linear structural causal models:

# Define SCM

X <- rnorm(100)

E_Y <- rnorm(100)

E_Z <- rnorm(100)

Y <- 2 + 1.5 * X + E_Y

Z <- 3 + 2 * X + 0.8 * Y + E_Z

# Estimate effects

lm(Y ~ X)

lm(Z ~ X + Y)

Call:

lm(formula = Y ~ X)

Coefficients:

(Intercept) X

1.971 1.719

Call:

lm(formula = Z ~ X + Y)

Coefficients:

(Intercept) X Y

3.0795 2.2095 0.8097

Interventional vs. Observational Data¶

Experimental Data:

Researchers randomly assign treatments

Groups are comparable (except for treatment)

Gold standard for causal inference

Example: Randomized controlled trial (RCT)

Observational Data:

Researchers observe naturally occurring variation

Groups may differ systematically (confounding)

Requires adjustment for valid causal inference

Example: Cohort study, case-control study

Key Difference:

Experimental: (randomization blocks confounders)

Observational: (confounding may be present)

Example: Shoe Size and Salary

Observational: People with larger shoes tend to have higher salaries

Reason: Gender affects both shoe size and salary (confounding)

Experimental: If we randomly assign shoe sizes, no effect on salary

Conclusion: No causal effect of shoe size on salary

Example - Ice Cream, Temperature, Emergencies:

Context: Observational data from 146 cities recording temperature (moderate/high), emergency calls (low/high), and ice cream sales (low/high).

Causal Graph:

Source

options(repr.plot.width = 6, repr.plot.height = 1)

library(gRbase)

dag.model <- dag(

c("IceCream","Temp"),

c("Emergency","Temp"))

par(mar = c(0.1, 0.1, 0.1, 0.1))

plot(dag.model)

Why Classical Model Finds Relationship:

Observation: Ice cream sales and emergency calls are positively associated

Reason: Temperature is a confounding variable - it affects both ice cream sales and emergency calls

Spurious correlation: The association is due to the common cause, not a direct causal effect

Conditional Probabilities:

# P(nEmergencies = high | IceCream = high)

(14 + 2) / 103 # 0.1553

# P(nEmergencies = high | IceCream = low)

(4 + 1) / 43 # 0.1163

# Risk ratio

0.1553 / 0.1163 # 1.34 times higherInterventional Probabilities:

do(IceCream = high) meaning: An intervention that sets ice cream sales to high for everyone, regardless of temperature or other factors.

Difference between P(Y|X) and P(Y|do(X)):

P(Y|X): Conditional probability - likelihood of Y among those who happened to have X

P(Y|do(X)): Interventional probability - likelihood of Y if we set X to a specific value

In most cases: P(Y|X) ≠ P(Y|do(X)) due to confounding

How the Graph Changes with do(IceCream = high):

The arrow from Temperature → IceCream is removed (intervention makes IceCream independent of Temperature)

Temperature still affects Emergency Calls directly

Calculating P(nEmergency = high | do(IceCream = high)): Using the adjustment formula:

# P(Temp = high) = 88/146 = 0.6027

# P(Temp = moderate) = 58/146 = 0.3973

# P(nEmergency = high | IceCream = high, Temp = high)

14 / (56 + 14) # 0.2000

# P(nEmergency = high | IceCream = high, Temp = moderate)

2 / (31 + 2) # 0.0606

# Interventional probability

0.2000 * 0.6027 + 0.0606 * 0.3973 # 0.1446Calculating P(nEmergency = high | do(IceCream = low)):

# P(nEmergency = high | IceCream = low, Temp = high)

4 / (14 + 4) # 0.2000

# P(nEmergency = high | IceCream = low, Temp = moderate)

1 / (24 + 1) # 0.0400

# Interventional probability

0.2000 * 0.6027 + 0.0400 * 0.3973 # 0.1498Causal Effect of IceCream on Emergency:

0.1446 - 0.1498 # -0.0052Conclusion: The estimated causal effect is approximately 0, suggesting no causal effect of ice cream sales on emergency calls. The observed association (1.34 times higher risk) is entirely due to confounding by temperature. This demonstrates why it’s crucial to distinguish between association and causation.

Instrumental Variables (IV)¶

When confounders are unmeasured, standard regression cannot estimate causal effects. Instrumental variables provide a solution.

Valid Instrument Z must satisfy:

Relevance: Z is associated with X (not too weak)

Exclusion restriction: Z has no direct effect on Y (only through X)

Independence: Z is independent of all confounders of X and Y

Two-Stage Least Squares (2SLS):

Regress X on Z to get predicted values

Regress Y on to estimate causal effect

library(AER)

# 2SLS using ivreg

iv.model <- ivreg(Y ~ X + W | Z + W, data = data)

summary(iv.model)Example: Education and Earnings

X: Education (years)

Y: Earnings

Z: Quarter of birth (affects education due to school entry age, but not earnings directly)

Assumption: Quarter of birth is independent of ability, family background, etc.

Counterfactual Reasoning¶

Counterfactuals answer questions like: “What would have happened if...?” for specific individuals.

Pearl’s Three-Step Method:

Abduction: Use observed data to infer the distribution of exogenous variables

Estimate the structural error terms from observed data

Action: Modify the structural equations to reflect the intervention

Set the variable of interest to its counterfactual value

Prediction: Use the modified model to predict the counterfactual outcome

Compute the new value based on the modified equations

Example - Online Sales Counterfactual:

Given observed: Visits = 179, Discount = 19%, Sales = 101 Question: What would sales be if Discount = 10%?

Estimated SCM from LiNGAM: Using the LiNGAM algorithm on historical sales data:

library(pcalg)

fit.sales <- lingam(dat_sales)

B <- round(fit.sales$Bpruned, 2)

colnames(B) <- rownames(B) <- colnames(dat_sales)

B

# sales adv visits discount

# sales 0 0.00 0.24 0.18

# adv 0 0.00 0.00 0.00

# visits 0 1.79 0.00 0.00

# discount 0 0.00 0.00 0.00Estimated DAG:

Adv → Visits (coefficient: 1.79)

Visits → Sales (coefficient: 0.24)

Discount → Sales (coefficient: 0.18)

No direct effect of Adv on Sales (only indirect through Visits)

Step 1 - Abduction:

# Estimate structural error for Sales

ES <- 101 - (55.65 + 0.24 * 179 + 0.18 * 19)

# ES = -1.03Step 2 - Action: Modify SCM for intervention do(Discount = 10):

Step 3 - Prediction:

visits <- 179 # Held constant (no intervention on visits)

discount <- 10 # Intervention

Sales <- 55.65 + 0.24 * visits + 0.18 * discount + ES

# Sales = 99.38Conclusion: If the discount had been 10% instead of 19%, they would have sold approximately 99 items (2 fewer than the observed 101).

Example - Pearl’s Three-Step Method: General template for counterfactual reasoning:

# Pearl's three-step method

# Step 1: Abduction

ES <- observed.Y - (beta0 + beta1 * observed.X)

# Step 2: Action

# Modify structural equation for intervention

# Step 3: Prediction

counterfactual.Y <- beta0 + beta1 * intervention.X + ESMarkov Equivalence¶

Markov Equivalence refers to the fact that different DAGs can represent the same conditional independence relationships.

Markov Equivalent Classes:

Chains and forks are Markov equivalent

CPDAGs (Completed Partially Directed Acyclic Graphs) represent equivalence classes

Example: The following DAGs are Markov equivalent (they encode the same conditional independencies):

All three imply:

Implications:

Without additional assumptions, we cannot distinguish between Markov equivalent DAGs from observational data alone

We need experimental data or strong assumptions to identify the true causal structure

Causal Structure Learning¶

Causal structure learning is the process of discovering causal relationships from data.

PC Algorithm (Peter & Clark, 1991)¶

The PC algorithm is a constraint-based method that:

Starts with a fully connected undirected graph

Tests for conditional independencies in the data

Removes edges where conditional independence is found

Orients edges based on v-structures (colliders)

library(pcalg)

# Create skeleton (undirected graph)

skeleton <- pc(data, alpha = 0.05)

# Orient edges

pc.fit <- pc(skeleton, data, alpha = 0.05)

# Visualize

plot(pc.fit)Assumptions:

Causal sufficiency: All common causes are measured

Causal Markov condition: D-separation implies conditional independence

Faithfulness: No independence relationships are “accidental”

LiNGAM Algorithm (Linear Non-Gaussian Acyclic Model)¶

LiNGAM identifies the full causal structure (not just Markov equivalence class) by assuming:

Linear relationships

Non-Gaussian errors

Acyclic structure

How it works: Uses Independent Component Analysis (ICA) to identify the causal order.

library(pcalg)

# Fit LiNGAM model

fit.lingam <- lingam(data)

# B matrix contains edge weights

B <- fit.lingam$Bpruned

colnames(B) <- rownames(B) <- colnames(data)

# Confidence intervals

ci <- fit.lingam$ci

# Visualize

plot(fit.lingam)Example: Online Sales Data

# Fit LiNGAM to sales data

fit.sales <- lingam(dat_sales)

B <- round(fit.sales$Bpruned, 2)

# Resulting DAG:

# Adv -> Visits -> Sales

# Discount -> Sales

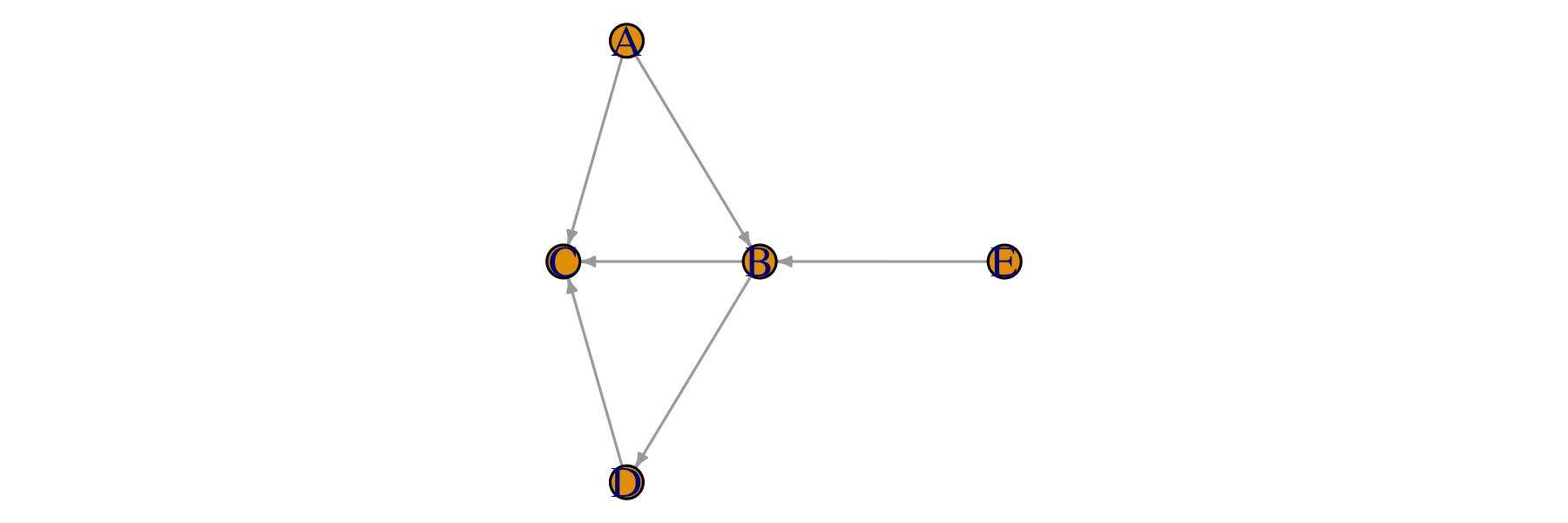

# (No direct effect of Adv on Sales, only through Visits)Source

options(repr.plot.width = 6, repr.plot.height = 1)

library(gRbase)

dag.model <- dag(

c("Sales","Visits", "Discount"),

c("Visits","Adv"))

par(mar = c(0.1, 0.1, 0.1, 0.1))

plot(dag.model)

Four Steps of Causal Inference¶

Step 1: Create a Causal Model

Use expert knowledge to specify a DAG

Represent all relevant variables and their causal relationships

Step 2: Identify the Causal Effect

Determine if the causal effect can be identified from observational data

Use d-separation and backdoor criterion to find valid adjustment sets

Step 3: Estimate the Causal Effect

Apply adjustment formula or other identification strategies

Use appropriate statistical methods (regression, matching, etc.)

Step 4: Test/Validate the Results

Check sensitivity to modeling assumptions

Test robustness to different specifications

Validate with external data if available